Spinal Surgery Products Market

Spinal Surgery Products Market Analysis By Device (Fusion Devices, Non-fusion Devices & Others) By Disease Indication (Degenerative Disc Disease, Complex Deformity, Traumas/Fractures & Others) By End-Use and By Region - Global Market Insights 2025 to 2035

Analysis of Spinal Surgery Products Market Covering 30+ Countries Including Analysis of US, Canada, UK, Germany, France, Nordics, GCC countries, Japan, Korea and many more

Spinal Surgery Products Market Outlook (2025 to 2035)

The spinal surgery products market is valued at USD 12.4 billion in 2025. As per Fact.MR’s analysis, the spinal surgery products industry will grow at a CAGR of 4.3% and reach USD 18.9 billion by 2035. This positive growth is powered by steady advancements in minimally invasive technology and a visible decline in spinal implant and surgical instrument costs.

In 2024, the spinal surgery products market witnessed a progressive transformation characterized by rapid adoption of minimally invasive procedures and increased dependence on sophisticated navigation systems. The industry witnessed a rise in elective spinal surgeries, especially in outpatient facilities, fueled by heightened patient awareness and the growing geriatric population.

Looking ahead to 2025, the industry will look to follow this growth trajectory, driven by innovation in non-fusion devices and AI-integrated surgical planning. Industry leaders will look to ramp up R&D spending and make strategic alliances to expand product portfolios and deepen global penetration. Further, with healthcare systems increasing focus on post-op recovery and long-term clinical effectiveness, industry demand for next-generation spinal devices and navigation-based products will improve consistently.

| Metric | Value |

|---|---|

| Industry Value (2025E) | USD 12.4 billion |

| Industry Value (2035F) | USD 18.9 billion |

| CAGR (2025 to 2035) | 4.3% |

Don't Need a Global Report?

save 40%! on Country & Region specific reports

Market Analysis

The spinal surgery devices industry is on a consistent growth trajectory, driven by the growing incidence of age-related spinal disorders and technological developments in minimally invasive surgery technologies. Growing usage of personalized and 3D-printed implants is fueling innovation in the industry. Players with robust R&D pipelines and outpatient care providers are set to gain the most, with companies lagging behind in embracing next-generation technology facing competitive disadvantage.

Top 3 Strategic Imperatives for Stakeholders

Accelerate Minimally Invasive Solutions

Invest in the growth of minimally invasive and navigation-assisted spinal solutions to address increasing demand for faster recovery and shorter hospital stays.

Focus on Patient-Centric Implant Personalization

Keep pace with the increasing trend of personalized care by broadening capability in 3D printing and patient-specific implant design to remain in advance of changing clinical demands.

Reinforce Strategic Partnerships and Global Presence

Seek mergers, acquisitions, and channel alliances to expand product offerings and reach emerging high-unmet-needs surgical sectors.

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability - Impact |

|---|---|

| Regulatory delays in expedited advanced spinal device approvals - Extended clearance times can hinder innovation deployment and limit revenue acceleration. | Medium - High |

| Slow uptake of advanced technologies in low-cost sectors - Monetary constraints and infrastructure shortcomings may hinder the incorporation of next-gen surgical devices. | High - Medium |

| Vulnerabilities in the supply chain hindering product continuity - Global sourcing issues and raw material shortages could undermine operational continuity and timely sector delivery. | Medium - Medium |

1-Year Executive Watch-List

| Priority | Immediate Action |

|---|---|

| Scale Precision Implant Solutions | Commissioned to develop advanced feasibility studies to increase production of bespoke 3D-printed spinal implants |

| Fortify Regulatory Navigation Framework | Establish strategic liaison initiatives with international regulatory bodies to facilitate approvals |

| Enhance Supply Chain Agility | Create diversified sourcing plans and regional supplier bases to provide assurance of continuity and responsiveness |

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

For the Boardroom

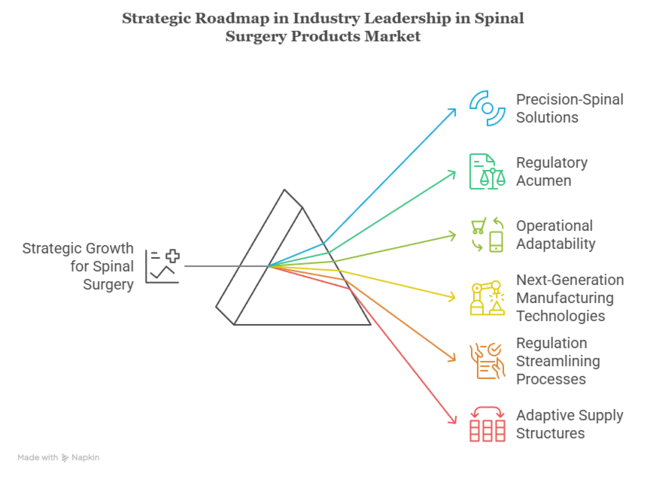

To stay ahead, companies need to reorient their growth plans on precision-spinal solutions, regulatory acumen, and operational adaptability. Increasing demand for minimally invasive treatments and customized implants indicates an unequivocal trend toward outcome-oriented care.

Investments in next-generation manufacturing technologies, regulation streamlining processes, and adaptive supply structures need to be prioritized by leadership. This insight demands an anticipatory roadmap-one that combines innovation with accessibility so that companies don't merely keep up but dictate the future of spinal surgery interventions.

Segment-Wise Analysis

By Devices

Fusion Devices are expected to be the most profitable segment in the spinal surgery products market between 2025 and 2035. This leadership is due to their extensive clinical application in managing severe spinal conditions like degenerative disc disease, spinal stenosis, and vertebral fractures-particularly among the elderly population.

Biomaterials innovation, improved spinal fusion methods, and increasing availability of minimally invasive fusion systems further fuel this segment's growth opportunity. Hospitals and surgery centers also are heavily investing in fusion-enabling navigation systems to enhance accuracy and minimize rates of complications.

Fact.MR study identified that the fusion devices category is expected to grow at a CAGR of around 4.7% during the period between 2025 and 2035 compared to other categories based on the clinical reliability and widening scope of applications.

By Disease Indication

Degenerative Disc Disease is anticipated to be the most profitable disease indication segment in the spinal surgery products industry during 2025-2035. This is largely attributed to the worldwide increase in the geriatric population, more sedentary life styles, and greater prevalence of spine-related degeneration in middle-aged individuals.

With patients opting for quicker recovery and permanent relief from chronic backache, surgical procedures-more so spinal fusion and disc replacement-are gaining prominence.

The chronic clinical burden of degenerative disc disease, in combination with innovation in motion-preserving technologies and biologic disc regeneration solutions, continues to draw significant investment and innovation in this area.

Fact.MR believes that the degenerative disc disease segment will expand at a strong CAGR of 4.9% during the period between 2025 and 2035, and it will be the top indication fueling long-term demand for spinal surgery products.

By End-Use

Hospitals are expected to be the most profitable end-use industry for spinal surgery devices from 2025 through 2035. This leadership is supported by their sophisticated infrastructure, presence of experienced surgeons, and capability of undertaking complicated and high-risk spinal surgeries that involve long preoperative and postoperative care. Hospitals also enjoy quicker uptake of high-cost, state-of-the-art technologies like robotic-assisted surgery and intraoperative imaging systems.

With increasing demand for minimally invasive and precision procedural care, hospitals remain ahead of the pack in terms of procedure volumes because of improved reimbursement systems and alignment with larger healthcare networks.

Fact.MR believes that the hospital segment will expand at a consistent CAGR of 4.6% during 2025-2035 with the help of ongoing investment in surgical innovation and holistic care provision.

Country-Wise Analysis

United States

The United States continues to be the prime center for spinal surgery innovation, fueled by high volumes of procedures, early adoption of minimally invasive procedures, and strong reimbursement models.

With a well-developed healthcare infrastructure and an increase in age-related spinal disorders, the need for sophisticated fusion and motion-preserving devices continues to gain momentum. The key players focus on the U.S. industry for introducing AI-integrated navigation systems and patient-specific implants.

Additionally, joint ventures between academic institutions and medtech firms are driving research in spinal biologics and regenerative medicine. Fact.MR forecasts that CAGR of United States will be 4.8% from 2025 to 2035.

India

India's spinal products industry is changing at a fast pace, driven by growing medical tourism, an aging population, and spurt in spine trauma due to road accidents.

Domestic players are now starting to move into the mid-end industry, with cost-effective yet technologically valid solutions. While robotic and navigation-assisted surgery adoption remains in its infancy, high-end urban hospitals are increasingly embracing these methods to address growing patient expectations.

Government-sponsored health programs and growth in multispecialty hospitals in Tier 2 and Tier 3 locations are expanding spine care access. Increasing awareness of degenerative spinal conditions and a shift towards surgical management from conservative management also continue to support this growth trend. Fact.MR opines that CAGR of India will be 4.5% from 2025 to 2035.

China

China is experiencing a dramatic shift in spinal surgery, fueled by a fast-growing aging population and robust government support for medtech innovation. The nation is heavily investing in local R&D and production of spinal implants to lower reliance on imports and improve affordability.

Urban hospitals are adopting smart surgery platforms and AI-based imaging systems, while the rural industry is getting improved access to quality spinal care through public-private partnerships. Spinal injury cases that are related to occupational risks are also propelling growing procedural demand.

The rise of China as a manufacturing center and hub for innovation is putting it on the map as a global actor in the spinal surgery industry. Fact.MR forecasts that CAGR of China will be 4.6% from 2025 to 2035.

United Kingdom

UK's spinal surgery industry is witnessing significant changes with added focus on value-based care and wait time reductions for elective operations. NHS change and private partnerships are facilitating rapid access to less invasive spinal surgery. Aging population and inactive lifestyle are driving the prevalence of spinal degeneration among working-age people.

The UK is also encouraging innovation in motion-sparing technologies and biodegradable implants with strategic collaborations between medtech companies and universities. A focus on clinical outcome monitoring and cost-effectiveness is fueling demand for high-performance implants with reduced hospital stays, even amid economic pressures. Fact.MR is of the opinion that CAGR UK will be 4.1% from 2025 to 2035.

Germany

Germany is an advanced industry for spinal surgery devices with powerful regulatory controls, a dense population of spine experts, and early take-up of sophisticated surgical methods. Demand for non-fusion and dynamic stabilization devices is increasing as a result of a preference for motion-preserving procedures. German companies are at the forefront of precision-engineered implants and are growing exports to neighboring European countries.

Furthermore, public health coverage of advanced spine procedures and postoperative rehabilitation enhances patient access. High health awareness and aging populations continue to drive volumes for procedures. Fact.MR opines that CAGR of Germany will be 4.2% from 2025 to 2035.

South Korea

South Korea is becoming a hub of excellence in spinal surgery, supported by tech-enabled healthcare infrastructure and rising medical tourism. The hospitals in the country are leaders in embracing robot-assisted spinal surgeries and AI-enabled navigation systems.

With an aging population and rising incidence of lumbar spinal stenosis, the demand for sophisticated fusion and interbody devices is on the rise.

Government funding of digital healthcare and reimbursement incentives for sophisticated surgical procedures are driving industry growth. Local firms are innovating at a rapid pace, introducing customized implants and next-generation surgical instruments to the industry. Fact.MR projects that CAGR of South Korea will be 4.4% from 2025 to 2035.

Japan

Japan's spine surgery industry is influenced by its super-aged society and intense emphasis on minimally invasive spine surgery. Hospitals are investing in small robotic systems appropriate for space-constrained operating rooms, whereas local companies concentrate on bioengineered implants and disc regeneration.

There is greater use of imaging-based preoperative planning to decrease complications and surgery time. Japan also has robust clinical trial networks for spinal devices, and thus it is a product testing and innovation hotspot.

The country's health insurance system facilitates advanced procedures, allowing greater patient access to high-end solutions. Japan's focus on clinical efficiency and care for the elderly make it a special growth environment. Fact.MR forecasts that CAGR of Japan will be 4.2% from 2025 to 2035.

France

France's spine surgery industry is gaining from the growth of specialized spine centers and the increasing use of robotics and AI in operating rooms. The public healthcare system makes access to advanced procedures more convenient, particularly in urban areas.

With patients seeking quicker recovery and shorter hospital stays, non-fusion procedures are becoming increasingly popular. French firms are expanding their presence in biodegradable implants and customized surgical planning software.

Inter-hospital and private manufacturer collaborative research is driving innovation in minimally invasive methods and image-guided systems. Better-trained surgeons, growing outpatient volumes, and expanding procedure volumes are continuing to support demand throughout the continuum of care. Fact.MR opines that CAGR of France will be 4.1% from 2025 to 2035.

Italy

Italy is witnessing progressive but consistent development in spinal surgeries, primarily due to increased consciousness regarding degenerative spine disorders and enhanced access for surgery through national healthcare reforms. Private healthcare service providers are upgrading their capabilities for minimally invasive and day-case spinal procedures.

Italian industry is investing in materials and modular design for implants with the aim to enhance procedural effectiveness and outcomes.

Greater interaction with European spine societies is speeding up knowledge exchange and innovation. Also, the nation is adopting digital platforms for preoperative evaluation and postoperative care, enhancing patient experience and readmission rates. Fact.MR is of the opinion that CAGR of Italy will be 4.0% from 2025 to 2035.

Australia-New Zealand

Australia-New Zealand is experiencing consistent growth in spinal surgery product uptake, backed by high per capita health spending and private healthcare network expansion. Surgeons throughout the region are adopting minimally invasive and motion-preserving solutions as part of regular care procedures. Patient-specific implants and 3D-printed devices are increasingly popular, especially among urban hospital settings.

Favorable regulatory environments and academia-industry collaborations are promoting clinical innovation and industry presence by global brands. With an aging population and increasing sports-related spinal trauma, the need for both non-fusion and fusion treatments is increasing. Cross-border partnerships and digital health platforms are also streamlining care provision. Fact.MR forecasts that CAGR of both the regions will be 4.3% from 2025 to 2035.

Fact.MR Survey Results: Spinal Surgery Products Industry Dynamics based on Stakeholder Perspectives

(Surveyed Q4 2024, n=480 stakeholders including surgeons, hospital procurement heads, device manufacturers, and outpatient facility operators across the US, Western Europe, Japan, and South Korea)

Key Priorities of Stakeholders

- Patient-Focused Outcomes: 84% of all worldwide respondents noted improved patient recovery time and surgical accuracy as among their highest clinical priorities.

- Minimal Invasive Techniques: 72% signalled a strategic push towards MIS-compatible devices to bring down hospital stay.

Regional Variation:

- US: 76% highlighted robot-assisted surgery integration, vs. 38% in Japan.

- Western Europe: 81% focused on integrating post-op data for reimbursement purposes.

- Japan/South Korea: 63% complained about compact instrumentation systems because of or spatial limitations, compared with 29% in the US.

The Acceptance of Advanced Technologies

Adoption Levels Depend on Infrastructure and ROI Expectations

- US: 62% of surgeons employ robotic guidance or intraoperative navigation systems, particularly in high-volume spine institutions.

- Western Europe: 53% use AI-based preoperative planning software, led by Germany (67%).

- Japan: 28% employ surgical robotics, attributing this to cost impediments and doctor conservativeness.

- South Korea: 41% have adopted augmented reality systems, particularly for lumbar fusion procedures.

ROI Divergence:

- Whereas 74% of US stakeholders see robotics as "worth the capital investment," just 33% in Japan see it as scalable.

Material and Design Preferences

Consensus:

- Titanium alloy continues to be the material of choice worldwide (69%) owing to strength, corrosion resistance, and MRI compatibility.

Regional Trends:

- Western Europe: 58% of procurement leaders favor bioresorbable polymers for certain fusion cases.

- South Korea/Japan: 44% chose PEEK-based implants due to reduced imaging artifacts and local production.

- US: 71% stuck with titanium, but interest in 3D-printed porous structures for improved osseointegration is on the rise.

Price Sensitivity

Common Challenges:

- 87% mentioned the rising cost of implantable devices and navigation technology as key challenges.

Regional Breakdown:

- US/Europe: 64% were willing to pay a 20–25% premium for bundled surgical platforms.

- Japan/South Korea: 73% required cost-optimized SKUs less than $6,000 per surgical set, and 49% insisted on government reimbursement.

- South Korea: 42% showed strong interest in robotic system rentals, compared to just 15% in the US.

Pain Points in the Value Chain

Manufacturers:

- US: 59% reported delays in FDA approvals for new spinal implants.

- Western Europe: 52% reported slow CE Mark alignment after Brexit.

- Japan: 61% wrestled with elderly surgeon demographics impacting adoption of sophisticated tools.

Distributors:

- US: 68% reported hospital value analysis committees (VACs) as top impediments for premium device approvals.

- Europe: 49% fought generic pricing pressure by Eastern European competitors.

- Japan/South Korea: 62% reported slow product turnover because of outdated OR infrastructure.

End-Users (Surgeons/Facilities):

- US: 45% reported insufficient surgical training on new platforms.

- Europe: 40% reported delays because of EMR-device interoperability gaps.

- Japan: 56% reported minimal rep support during procedures.

Future Investment Priorities

Global Alignment:

- 77% of world manufacturers are gearing up to invest in AI-powered surgical systems.

Regional Priorities:

- US: 65% emphasized data-integrated implants with capabilities for post-op analytics and remote monitoring.

- Western Europe: 60% put emphasis on carbon-neutral device production and recyclable packaging.

- Japan/South Korea: 51% set target towards miniaturized systems specific to aging patients and reduced anatomies.

Regulatory Impact

- US: 66% find that CMS coding reforms for outpatient spine surgeries are reforming procurement plans.

- Western Europe: 79% see MDR-compliance as fueling design innovation and device responsibility.

- Japan/South Korea: A mere 35% envisioned regulations as making a difference with reference to lackadaisical enforcement and slow policy development.

Conclusion: Deviation vs. Consensus

- High Consensus: Patient-centred outcomes, durability, and digital surgical integration are core for global approaches.

Key Deviations:

- US: Innovation through robotics and AI.

- Europe: Sustainability-driven designs and reimbursement synergies.

- Asia: Pragmatic innovation with spacial, financial, and diffusion hurdles.

Strategic Insight:

- Regional subtlety-robotics in the US, green tech in Europe, and small devices in Asia-will dictate competitive advantage.

Government Regulations

| Country | Regulatory Impact |

|---|---|

| US | FDA approval under 510(k) or PMA routes is mandatory; CMS reimbursement reforms for outpatient spine surgeries are accelerating adoption of cost-efficient devices. |

| India | CDSCO classifies spinal implants as Class C/D devices, requiring import licenses and local clinical evidence; pricing caps via NPPA impact premium device sales. |

| China | NMPA mandates local clinical trials for spinal products; domestic preference policies favor homegrown brands under the "Made in China 2025" strategy. |

| UK | Post-Brexit divergence from EU MDR has introduced dual pathways; UKCA marking now required for spinal devices sold after July 2025. |

| Germany | EU MDR compliance is non-negotiable, with emphasis on clinical evidence and traceability; reimbursement tied to HTA evaluations by G-BA. |

| South Korea | MFDS approval necessary, with increased scrutiny on imported implants; price-volume agreements restrict premium product penetration. |

| Japan | PMDA enforces rigorous post-industry surveillance; foreign firms must collaborate with local MAHs (Marketing Authorization Holders). |

| France | HAS (Health Authority) mandates HTA for public reimbursement; compliance with EU MDR and environmental impact assessments is key. |

| Italy | EU MDR compliance enforced strictly; regional procurement bodies heavily influence public hospital purchases, favoring cost-effective models. |

| Australia-New Zealand | TGA (Australia) and Medsafe (NZ) require CE/FDA equivalence and post-market safety data; growing push for regional manufacturing incentives. |

Competitive Landscape

The industry for spinal surgery products is moderately consolidated, with a few industry leaders holding a large share of the global industry. Major players compete on the basis of innovation in spinal implants and navigation systems, strategic acquisition, price competitiveness, and emerging sector expansion.

One of the major differentiators has been the capability to design technologically superior products like 3D-printed implants and minimally invasive surgery instruments, with companies also matching offerings to changing clinical preferences and regulatory requirements.

In 2024, some significant events revamped the competitive framework. Stryker revealed a plan to spin off its American spinal business into the hands of Viscogliosi Brothers following underperformance within this group, which accrued quarterly revenue worth $186 million and recorded the weakest growth within the company portfolio (3.2%).

Moreover, in March 2025, India-based Zydus Lifesciences revealed a €256.8 million acquisition of 85.6% ownership of France's Amplitude Surgical, strengthening its push into the European orthopedic and spinal devices sector.

These moves by industry leaders show that the landscape is changing where competitive advantage in the spinal surgery products industry is shaped by innovation, regulatory flexibility, and international growth.

Market Share Analysis

- Medtronic (25-30%) - Leads with full-line spinal implants, navigation, and biologics.

- Johnson & Johnson [DePuy Synthes] (20-25%) - Dominant in minimally invasive (MIS) and motion-preservation technologies.

- Stryker (15-20%) - Leader in robotic spine surgery (SpinePro) and 3D-printed implants.

- Zimmer Biomet (10-15%) - Concentrates on spinal fusion solutions and AI-powered surgical planning.

- NuVasive (8-12%) - Expert in lateral access surgery and intraoperative monitoring.

- Globus Medical (5-10%) - Disruptor with robotic platforms (ExcelsiusGPS) and expandable implants.

Key Industry Players Include

- Medtronic

- Johnson & Johnson (DePuy Synthes)

- Stryker Corporation

- Zimmer Biomet

- Globus Medical

- NuVasive

- RTI Surgical

- Orthofix Medical

- Alphatec Holdings

- SeaSpine Holdings

- B. Braun Melsungen AG

- Ulrich GmbH & Co. KG

- Aesculap (B. Braun subsidiary)

- Wenzel Spine

- Spineart SA

Segmentation

Segmentation by Device:

Fusion Devices, Non-fusion Devices, Others

Segmentation by Disease Indication:

Degenerative Disc Disease, Complex Deformity, Traumas & Fractures, Others

Segmentation by End Use:

Hospitals, Ambulatory Surgery Centers, Specialty Clinics, Others

Segmentation by Region:

North America, Latin America, Europe, East Asia, South Asia & Oceania, Middle East and Africa (MEA), North America

Table of Content

- 1. Global Market - Executive Summary

- 2. Global Market Overview

- 3. Market Risks and Trends Assessment

- 4. Market Background and Foundation Data Points

- 5. Global Market Demand (US$ Mn) Analysis 2020 to 2024 and Forecast, 2025 to 2035

- 6. Global Market Analysis 2020 to 2024 and Forecast 2025 to 2035, By Device

- 6.1. Fusion Devices

- 6.2. Non-fusion Devices

- 6.3. Others

- 7. Global Market Analysis 2020 to 2024 and Forecast 2025 to 2035, by Disease Indication

- 7.1. Degenerative Disc Disease

- 7.2. Complex Deformity

- 7.3. Traumas & Fractures

- 7.4. Others

- 8. Global Market Analysis 2020 to 2024 and Forecast 2025 to 2035, by End Use

- 8.1. Hospitals

- 8.2. Ambulatory Surgery Centers

- 8.3. Specialty Clinics

- 8.4. Others

- 9. Global Market Analysis 2020 to 2024 and Forecast 2025 to 2035, by Region

- 9.1. North America

- 9.2. Latin America

- 9.3. Europe

- 9.4. East Asia

- 9.5. South Asia & Oceania

- 9.6. Middle East and Africa (MEA)

- 10. North America Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- 11. Latin America Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- 12. Europe Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- 13. East Asia Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- 14. South Asia & Oceania Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- 15. Middle East and Africa Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- 16. Market Structure Analysis

- 17. Competition Analysis

- 17.1. Medtronic

- 17.2. Johnson & Johnson (DePuy Synthes)

- 17.3. Stryker Corporation

- 17.4. Zimmer Biomet

- 17.5. Globus Medical

- 17.6. NuVasive

- 17.7. RTI Surgical

- 17.8. Orthofix Medical

- 17.9. Alphatec Holdings

- 17.10. SeaSpine Holdings

- 17.11. B. Braun Melsungen AG

- 17.12. Ulrich GmbH & Co. KG

- 17.13. Aesculap (B. Braun subsidiary)

- 17.14. Wenzel Spine

- 17.15. Spineart SA

- 18. Assumptions And Acronyms Used

- 19. Research Methodology

Don't Need a Global Report?

save 40%! on Country & Region specific reports

List Of Table

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

List Of Figures

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

- FAQs -

What is fueling growth in the spinal surgery products industry?

Increasing incidence of degenerative spine conditions and advancements in minimally invasive procedures are fueling industry growth.

Which technologies are transforming the spinal surgery industry?

3D printing, robotic surgery, and AI-powered navigation systems are transforming spinal procedures.

How are manufacturers adapting to regulatory pressures?

Firms are adapting by ensuring compliance through certification alignment and investment in safer, evidence-based device innovation.

Is there a change in demand in end-use environments?

Yes, ambulatory surgery centers and outpatient are experiencing greater adoption as a result of faster recovery models and cost savings.

What is the role of global players in regional dynamics?

Strategic partnerships and acquisitions of regional companies by major players are deepening geographic penetration and diversifying portfolios.

Spinal Surgery Products Market