Point of Care Diagnostics Market

Point of Care Diagnostics Market Trend Analysis Based on Platform, Application, End-User, and Region 2025 to 2035

Analysis of Point of Care Diagnostics Market Covering 30+ Countries Including Analysis of US, Canada, UK, Germany, France, Nordics, GCC countries, Japan, Korea and many more

Point of Care Diagnostics Market Outlook (2025 to 2035)

The Point of Care diagnostics market is valued at USD 44.7 billion in 2025. As per Fact.MR's analysis, the sector will grow at a CAGR of 7% and reach USD 87.9 billion by 2035.

Reflecting on 2024, the sector witnessed a dramatic development, propelled by the progress made by rapid testing technology and the broader adoption of decentralized healthcare solutions.

The escalating need for near-patient and home-based diagnostics devices contributed significantly to defining the sector's development landscape. Additionally, the escalating fears about infectious and chronic ailments assisted in initiating investment in new-generation diagnostic devices, boosting the sector's growth in developed as well as developing countries.

Moving forward to 2025, the industry is set to continue growth as technological integration continues to improve point-of-care testing accuracy and efficiency.

Greater investment in research and development, together with regulatory endorsement of streamlined approval procedures, is likely to hasten product innovation. Furthermore, the growing popularity of digital health solutions and AI-based diagnostics is set to increase adoption in all healthcare settings.

| Metric | Value |

|---|---|

| Industry Value (2025E) | USD 44.7 billion |

| Industry Value (2035F) | USD 87.9 billion |

| CAGR (2025 to 2035) | 7% |

Don't Need a Global Report?

save 40%! on Country & Region specific reports

Market Analysis

The Point of Care diagnostics sector is heading for a solid growth path, stimulated by growing demand for rapid and decentralized testing solutions and technological progress in diagnostics.

Major beneficiaries are healthcare providers, device manufacturers for diagnostics, and patients who are looking for quicker and easier access to testing.

In contrast, conventional laboratory-based testing centers might suffer from changing preferences. With intensifying innovation and regulatory support, the industry is poised to grow exponentially in all of the world's healthcare sectors.

Top 3 Strategic Imperatives for Stakeholders

Utilize AI for Accuracy and Velocity

Apply AI-based diagnostics to enhance accuracy, accelerate results, and enhance accessibility in decentralized healthcare environments.

Move Proactively through Regulatory Environments

Place innovations alongside shifting compliance needs and evolving healthcare needs to accelerate sector entry and maintain a competitive edge.

Create High-Impact Partnerships

Deepen partnerships with healthcare providers, retail pharmacies, and digital health platforms to facilitate distribution at scale, enhance adoption, and extend sector reach.

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability - Impact |

|---|---|

| Regulatory Volatility - Changing compliance requirements can slow down approvals and hamper industry growth. | High - Severe |

| Supply Chain Risks - Material shortages and supply chain bottlenecks may interfere with production and distribution. | Moderate - High |

| Rapid Technological Displacement - Rapid innovation can obsolete current solutions, affecting competitiveness. | High - Critical |

1-Year Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Next-Gen Diagnostic Innovation | Accelerate AI-facilitated testing innovations to enhance accuracy and scalability. |

| Regulatory Foresight & Adaptation | Enhance regulatory intelligence and advocacy to expedite approvals. |

| Supply Chain Fortification | Enlarge supplier networks and institute risk-mitigation systems to guarantee stability. |

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

For the Boardroom

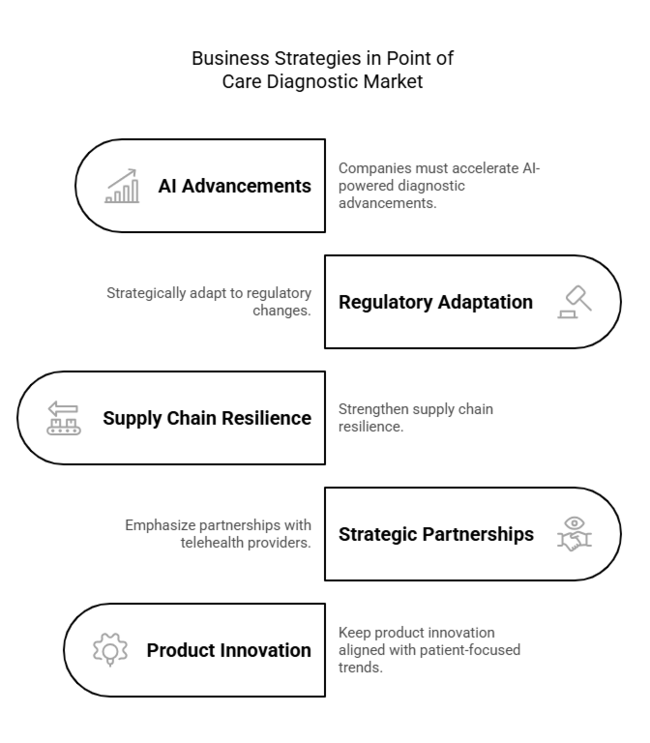

To stay ahead, companies must accelerate AI-powered diagnostic advancements, strategically adapt to regulatory changes, and strengthen supply chain resilience. Amidst fast-evolving decentralized healthcare, companies must emphasize strategic partnerships with telehealth providers and retail networks to enhance accessibility.

This insight highlights the imperative of keeping product innovation aligned with evolving patient-focused trends, in order to maintain long-term industry leadership in a rapidly digital and demand-driven environment.

Segment-Wise Analysis

By Platform

The development of Point of Care diagnostics on many different platforms will force innovation and optimization between the years 2025 and 2035. Lateral flow tests will persistently dominate in response to affordability and simplicity, especially in detecting infectious diseases.

Microfluidics and molecular diagnosis will see their implementation accelerate due to AI-inspired technology and miniaturization for the purpose of maximizing accuracy.

Immunoassays will become increasingly popular in chronic disease monitoring, whereas dipsticks will continue to be an affordable choice in developing economies.

With increasing demand for decentralized healthcare, the platform segment will grow at a CAGR of around 6.8% driven by ongoing technological developments and regulatory favor for quicker approvals of diagnostics.

By Application

Growing applications in Point of Care diagnostics will revolutionize healthcare accessibility and efficiency during the forecast period.

Glucose monitoring will experience steady growth as diabetes cases increase globally, and cardiometabolic and cholesterol testing will pick up speed because of the increasing incidence of lifestyle diseases.

Infectious disease diagnostics will continue to be crucial, especially with the growing emphasis on rapid testing and early diagnosis. Pregnancy and fertility testing will keep transforming with the integration of digitization, and hematology and urinalysis testing will be bolstered by automation for more accurate outcomes.

Increasing demand for real-time diagnostics in a wide range of healthcare environments will drive this segment's CAGR to approximately 7.2%, guaranteeing continued adoption across various clinical and non-clinical purposes.

By End User

The use of Point of Care diagnostics in various healthcare environments will increase from 2025 to 2035. Hospitals will still have a substantial proportion because the requirement for instantaneous diagnostic information will continue in emergency and inpatient settings.

Diagnostic laboratories will include more decentralized testing solutions, with enhanced efficiency and turnaround times. Clinics and physician offices will fuel demand for small, quick diagnostic devices to facilitate quicker patient management.

Home care testing will grow significantly, aided by the increasing demand for self-monitoring solutions and telehealth integration. The industry will progress at a CAGR of around 7.5%, fueled by rising investments in personalized healthcare and the transition towards patient-centric diagnostic models.

Country-Wise Analysis

United States

The United States diagnostics industry will experience consistent growth, fueled by the increased focus on decentralized healthcare, technological advancements, and mounting pressure for quick testing solutions.

The presence of leading industry players and an established regulatory landscape will further speed up the implementation of AI-based diagnostic technologies, especially in managing chronic diseases.

Personalized care and home diagnostics will see a boost, responding to demands for real-time, patient-specific solutions.

With the integration of telehealth going deeper, the industry will see a definite push toward automation and interoperability of diagnostic equipment. Development in molecular diagnostics and real-time monitoring of diseases will keep the industry's growth going.

Fact.MR forecasts that the CAGR of point of care diagnostics in the United States will be 7.3% by 2035.

India

The Indian diagnostics sector will see a revolutionary change as healthcare access increases and government policies drive the push for low-cost, technology-based solutions.

Increasing demand for infectious disease testing, driven by heightened awareness and frequent outbreaks, will spur industry penetration. Increases in the adoption of mobile health (mHealth) solutions and artificial intelligence-driven diagnostic platforms will increase rural healthcare outreach.

The emergence of self-monitoring diagnostics, especially for cardiovascular conditions and diabetes, will be responsible for fueling innovation in home-care testing. Investment in diagnostic startups by the private sector and strategic partnerships with international companies will further spur industry growth.

Fact.MR is of the opinion that the CAGR of point of care diagnostics in India would be 7.8% by 2035.

China

The point of care diagnostics industry of China will witness tremendous growth because of the widespread adoption of AI, automation, and smart healthcare solutions. The next-generation molecular testing and laboratory-on-a-chip technology will lead the prominent hospital facilities and city healthcare centers.

Furthermore, the nation’s rising aging population and continuous incidence of chronic diseases will thrive the demand for real-time health monitoring solutions. Increased insurance coverage and public-private partnerships will further expand industry penetration, making diagnostic services more accessible to rural communities.

Digitalization and data-driven healthcare services will develop a seamless ecosystem for quicker diagnostics and patient management.

Fact.MR projects that the CAGR of point of care diagnostics in China will be 7.6% by 2035.

United Kingdom

The Point of Care diagnostics industry in the United Kingdom will flourish as the nation is persistently investing in digital healthcare infrastructure and AI-based diagnostic innovations. The National Health Service (NHS) will be instrumental in speeding up the uptake of portable testing products, especially for infectious diseases and cardiovascular diseases.

Increasing patient inclination towards home-based diagnostics and preventive health checks will further accelerate industry growth. The convergence of cloud-based diagnostic platforms with telehealth solutions will increase remote patient monitoring functions.

Strategic partnerships between research centers and biotech companies will give rise to innovative advancements in real-time disease diagnosis.

Fact.MR forecasts that the CAGR of point of care diagnostics in the United Kingdom will grow at 7.2% over the forecast period.

Germany

The German industry will be driven by robust R&D spends, automation, and precision medicine solutions. Next-generation diagnostic development in the country will take microfluidic-based testing and AI-based molecular diagnostics to the forefront, with rapid and decentralized testing in emergency care applications growing in demand.

The healthcare industry's move toward personalized medicine and real-time monitoring solutions will fuel growth.

Collaboration between research institutions and medical technology companies will result in ongoing product development, while regulation will facilitate quicker approvals of advanced diagnostic products.

Fact.MR opines that the CAGR of point of care diagnostics in Germany would be 7.4% between 2025-2035.

South Korea

South Korea's Point of Care diagnostics industry will grow strongly as a result of its strong biotechnology sector and high penetration of smart healthcare solutions.

Diagnostic algorithms driven by artificial intelligence and nanotechnology-based testing kits will be more prominent, especially in monitoring infectious diseases and metabolic disorders. Government support for local production and innovation in molecular diagnostics will improve domestic production capacities.

Solid digital health infrastructure and strategic partnerships between medical technology companies and AI developers will also further boost the industry's growth path.

Fact.MR projects that the CAGR of point of care diagnostics in South Korea will be 7.5% from 2025 to 2035.

Japan

Japan's diagnostics sector will evolve through its technological leadership and miniaturized diagnostic capabilities. The nation's emphasis on automation and robot-based healthcare will lead to the creation of highly efficient, AI-based diagnostic products.

A high and growing incidence of chronic disease, especially in diabetes and cardiovascular management, will propel demand. Spending on wearable diagnostics and advanced biosensors will drive industry growth.

Government policies encouraging the early detection of illnesses and early diagnostics at home will further enhance adoption. Interconnected collaborations among academics and industrial players will enable constant innovation on intelligent diagnostic platforms.

Fact.MR forecasts that the CAGR of point of care diagnostics in Japan would reach 7.3% from 2025 to 2035.

France

France's Point of Care diagnostics industry will continue to increase gradually as the nation focuses on updating its health care infrastructure. There will be a dramatic upsurge in the use of real-time diagnosis in emergency care and primary care settings, promoted by improvements in AI and molecular diagnostics. Investment in biotechnology startups will help to drive next-generation rapid-testing technology.

Government initiatives favoring local production of diagnostic equipment will increase self-reliance and availability. The increasing significance of early disease diagnosis and precision medicine will drive demand for sophisticated POC solutions in hospitals and home care environments.

Fact.MR is of the opinion that sales will grow at a CAGR of 7.1% in France.

Italy

Italy's Point of Care diagnostics industry will witness significant growth owing to greater focus on personalized medicine and preventive diagnosis. Growing healthcare spending and the uptake of digital health technologies will further fuel demand for rapid testing technologies.

Growth in telemedicine and remote patient monitoring services will drive extensive adoption of home-based diagnostics.

Public-private partnerships in R&D will enable ongoing technological innovation, especially in point-of-care molecular testing. The sector will gain from government-supported initiatives that drive domestic manufacturing and innovation of diagnostic solutions.

Fact.MR opines that the CAGR of point of care diagnostics in Italy would reach 7.2% by 2035.

Australia & New Zealand

The Australian and New Zealand diagnostics sector will experience fast-paced growth with solid government support in digital health and cutting-edge diagnostics.

The rise in demand for remote testing products in rural and underserved areas will propel innovation. The growth of wearable diagnostics and AI-supported screening products will improve early detection and treatment of diseases.

Self-monitoring solution-promoting public health initiatives will drive the implementation of home-based diagnostics.

Strategic collaborations among healthcare providers, research organizations, and technology firms will be vital to industry growth.

Fact.MR forecasts that the CAGR of point of care diagnostics in Aus-Nz will be 7.3% from 2025 to 2035.

Fact.MR Survey Results: Point of Care Diagnostics Industry Dynamics Based on Stakeholder Perspectives

(Surveyed Q4 2024, n=500 stakeholder participants evenly distributed across manufacturers, healthcare providers, diagnostic laboratories, and distributors in the US, Western Europe, Japan, South Korea, and India.)

Key Priorities of Stakeholders

- Adherence to Regulatory Standards: 84% of stakeholders across the world ranked complying with changing diagnostic regulations, such as rapid test accuracy and data protection, as a "critical" priority.

- Speed and Accuracy: 78% indicated the importance of high-sensitivity diagnostics to reduce false negatives and enhance treatment effectiveness.

Regional Variance:

- US: 71% of healthcare professionals ranked AI-based diagnostics for real-time decision-making compared to 48% in Japan.

- Western Europe: 87% emphasized sustainability (biodegradable test materials, minimized medical waste) as a major consideration, versus 52% in South Korea.

- India: 69% of the respondents emphasized affordability and cost-efficient rapid test solutions, considering the necessity for mass accessibility, versus 29% in Western Europe.

Adopting Advanced Technologies

High Variance:

- US: 60% of healthcare professionals embraced cloud-integrated diagnostics for remote patient monitoring, fueled by telehealth growth.

- Western Europe: 54% had invested in automated molecular diagnostic platforms, led by Germany (66%) because of strict EU regulations.

- Japan: A mere 24% included AI-fortified diagnostics, attributing this to expense and "overcomplexity" for small-volume clinics.

- India: 47% had invested in mobile-based POC diagnostics to increase rural accessibility compared to 22% in the US.

Convergent and Divergent Views of ROI

- 73% of American stakeholders concluded automation in diagnostics was "worth the investment," while 40% of Japanese stakeholders continued to use manual testing kits.

Material Choices

Consensus:

- Microfluidics and Polymer-Based Cartridges: Chosen by 67% of users for increased portability and affordability.

Variation:

- Western Europe: 59% used environment-friendly biodegradable test strips, more than the world average of 38%.

- Japan/South Korea: 43% chose hybrid polymer-glass substrates due to improved stability of tests under humid environments.

- US: 68% ranked the high-density plastic-based diagnostic kits, but 27% of the East Coast hospitals indicated a trend toward glass microfluidic devices for accuracy testing.

Price Sensitivity

Shared Challenges:

- Escalating production costs due to supply chain disruptions and increasing material prices were mentioned by 89% of the respondents.

Regional Differences:

- US/Western Europe: 64% would pay a 15–20% premium for diagnostics and automation with AI integration.

- Japan/South Korea: 76% preferred lower-cost models (<$3,000 per unit) with few software add-ons.

- India: 82% weighed in on affordability, with a need for low-cost test kits below $500 for mass deployment.

Leasing vs. Upfront Investment:

- South Korea: 49% of hospitals showed interest in leasing diagnostic equipment to control costs, compared with 21% in the US.

Pain Points in the Value Chain

Manufacturers:

- US: 57% experienced pain due to semiconductor shortages impacting chip-based diagnostic devices.

- Western Europe: 50% mentioned delays in regulatory approvals under the EU In Vitro Diagnostic Regulation (IVDR).

- India: 63% pointed out the absence of local manufacturing infrastructure, growing dependency on imports.

Distributors

- US: 72% indicated supply chain delays from foreign component sourcing.

- Western Europe: 55% mentioned competition from lower-cost Asian diagnostic producers.

- Japan/South Korea: 61% experienced delayed distribution in rural healthcare centers.

End-Users (Healthcare Providers & Laboratories):

- US: 46% mentioned excessive software maintenance costs for AI-enabled diagnostics.

- Western Europe: 41% encountered challenges integrating new devices with existing healthcare IT systems.

- India: 59% mentioned inadequate technical training for healthcare workers operating advanced POC devices.

Priorities for Future Investment

Alignment:

- 75% of worldwide manufacturers intend to make more investments in AI-based diagnostics and next-generation biosensors.

Divergence:

- US: 63% were interested in scaling up lab-on-a-chip technology for multi-disease screening.

- Western Europe: 58% were interested in sustainable manufacturing processes, including energy-efficient diagnostic production.

- India: 52% were interested in mobile-integrated diagnostics to improve access in underserved areas.

Regulatory Influence

- US: 70% of stakeholders reported that changing FDA regulations for AI-enabled diagnostics had a significant influence on product development timelines.

- Western Europe: 83% saw the EU's IVDR regime as both a compliance hurdle and a premium-quality diagnostics driver.

- Japan/South Korea: Just 35% believed regulations had significant influence over procurement, attributing to lenient enforcement versus Western sectors.

- India: 69% recognized the value of streamlined government approvals to drive domestic diagnostic device production.

Conclusion: Variance vs. Consensus

High Consensus:

- Global stakeholders were in agreement on the imperative of compliance with changing diagnostic regulations, cost-efficient innovation, and AI integration.

Key Variances:

- US: Automation- and AI-powered growth, contrasted with Japan/South Korea: Cost-efficient manual testing over solutions.

- Western Europe: Innovation for sustainability, contrasted with India: Affordability and mobile-friendly diagnostics demand.

Strategic Insight:

- One size will not fit all. Regionalization-US with AI and automation, Europe with sustainability, Asia with cost-efficient models-is required to access sector potential.

Government Regulations

| Country | Regulatory Impact & Mandatory Certifications |

|---|---|

| United States | The FDA requires 510(k) clearance or PMA approval for point-of-care diagnostics. CLIA waivers are necessary for outside-laboratory use. Tighter regulation is in the offing for AI-based diagnostics. |

| India | CDSCO categorizes diagnostics into risk level, and approvals are needed for Class C & D devices. BIS certification is required for domestic manufacture. "Make in India" promotes local manufacturing. |

| China | NMPA places stringent pre-market approvals on domestic and imported diagnostics. Class III also has stringent clinical validation requirements. |

| United Kingdom | UKCA marking has taken the place of CE certification post-Brexit. MHRA controls device approval with an increasing emphasis on data security in diagnostics. |

| Germany | EU IVDR compliance is required, requiring significant clinical evidence for approval. High-risk diagnostics must comply with stringent MDR regulations. |

| South Korea | The MFDS classifies diagnostics by risk, mandating in-country clinical trials for high-risk devices. Government subsidies incentivize AI-diagnostics. |

| Japan | PMDA regulates device approvals, mandating domestic trials for overseas diagnostics. The government supports digital health integration in diagnostics. |

| France | EU IVDR compliance is mandatory. HAS analyzes cost-effectiveness of diagnostics prior to reimbursement approval. |

| Italy | Strict EU IVDR regulations apply. National health authorities stress interoperability of digital diagnostic solutions in healthcare networks. |

| Australia-New Zealand | The TGA (Australia) and Medsafe (New Zealand) need sector approval under risk-based categories. Fast-track authorizations are available for critical diagnostics. |

Competitive Landscape

The industry for point-of-care diagnostics is relatively fragmented, with many players competing for industry share through various efforts.

Leading players compete on competitive pricing, quick innovation (AI, handheld devices), strategic alliances (with hospitals, laboratories), and geographic expansion (particularly in emerging sectors). Growth strategies involve M&A to gain market share, new product launches for quicker diagnostics, and obtaining regulatory approvals for reimbursement.

In March 2024, Sonic Healthcare increased its dominance in Australia by acquiring Australian Clinical Labs' pathology business for $750 million, strengthening its sector position.

Abbott gained FDA approval in April 2024 for its high-sensitivity troponin test, enhancing the ability to detect heart attacks early. In addition, in June 2024, Roche launched a rapid HPV test to make cervical cancer screening more accessible to low-resource settings.

Also, in January 2024, there was a significant collaboration between Siemens Healthineers & Mayo Clinic. The partnership is to create AI-based point-of-care diagnostics for critical care environments.

Market Share Analysis

- Roche Diagnostics (~20%) - Leads with high-end immunoassays and molecular POC platforms.

- Abbott Laboratories (~18%) - Dominates in rapid testing (e.g., BinaxNOW, i-STAT).

- Siemens Healthineers (~12%) - Strong presence in hospital-based POC with Atellica® solutions.

- Thermo Fisher Scientific (~10%) - Growing in infectious disease and critical care testing.

- QuidelOrtho (~8%) - Specializes in flu, COVID-19, and respiratory testing.

- BD (Becton Dickinson) (~7%) - Major player in POC microbiology and diabetes monitoring.

Key Industry Players Include

- Hoffmann-La Roche Ltd.

- Abbott Laboratories

- Siemens Healthineers (Siemens AG)

- Danaher Corporation (Beckman Coulter, Cepheid, Radiometer)

- Thermo Fisher Scientific Inc.

- BD (Becton, Dickinson and Company)

- bioMérieux SA

- QuidelOrtho

- Johnson & Johnson Services Inc.

- Nova Biomedical

- Cardinal Health Inc.

- Bio-Rad Laboratories Inc.

- Sysmex Corporation

- EKF Diagnostics (part of Citadel Group)

- Sekisui Diagnostics

Segmentation

By Platform:

Lateral Flow Assays, Dipsticks, Microfluidics, Molecular Diagnostics, Immunoassays, Others

By Application:

Glucose Monitoring Products, Cardiometabolic Monitoring Products, Infectious Disease Testing Products, Pregnancy & Fertility Testing Products, Urinalysis Testing Products, Cholesterol Testing Products, Hematology Testing Products, Drugs-of-Abuse Testing Products, Others

By End User:

Hospitals, Diagnostic Laboratories, Clinics/Physician Offices, Home Care, Others

By Region:

North America, Latin America, Europe, East Asia, South Asia & Oceania, Middle East and Africa (MEA)

Table of Content

- Global Market - Executive Summary

- Global Market Overview

- Market Risks and Trends Assessment

- Market Background and Foundation Data Points

- Global Market Demand (US$ Bn) Analysis 2020 to 2024 and Forecast, 2025 to 2035

- Global Market Analysis 2020 to 2024 and Forecast 2025 to 2035, By Platform

- Lateral Flow Assays

- Dipsticks

- Microfluidics

- Molecular Diagnostics

- Immunoassays

- Others

- Global Market Analysis 2020 to 2024 and Forecast 2025 to 2035, by Application

- Glucose Monitoring Products

- Cardiometabolic Monitoring Products

- Infectious Disease Testing Products

- Pregnancy & Fertility Testing Products

- Urinalysis Testing Products

- Cholesterol Testing Products

- Hematology Testing Products

- Drugs-of-abuse Testing Products

- Others

- Global Market Analysis 2020 to 2024 and Forecast 2025 to 2035, by End User

- Hospitals

- Diagnostic Laboratories

- Clinics/Physician Offices

- Home Care

- Others

- Global Market Analysis 2020 to 2024 and Forecast 2025 to 2035, by Region

- North America

- Latin America

- Europe

- East Asia

- South Asia & Oceania

- Middle East and Africa (MEA)

- North America Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- Latin America Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- Europe Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- East Asia Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- South Asia & Oceania Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- Middle East and Africa Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- Market Structure Analysis

- Competition Analysis

- Hoffmann-La Roche Ltd.

- Abbott Laboratories

- Siemens Healthineers (Siemens AG)

- Danaher Corporation (Beckman Coulter, Cepheid, Radiometer)

- Thermo Fisher Scientific Inc.

- BD (Becton, Dickinson and Company)

- bioMérieux SA

- QuidelOrtho

- Johnson & Johnson Services Inc.

- Nova Biomedical

- Cardinal Health Inc.

- Bio-Rad Laboratories Inc.

- Sysmex Corporation

- EKF Diagnostics (part of Citadel Group)

- Sekisui Diagnostics

- Assumptions And Acronyms Used

- Research Methodology

Don't Need a Global Report?

save 40%! on Country & Region specific reports

List Of Table

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

List Of Figures

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

- FAQs -

What's propelling the rapid growth of point-of-care diagnostics?

Advances in microfluidics, increasing needs for real-time disease monitoring, and decentralized healthcare embracement are driving industry change.

How are top companies gaining a competitive advantage?

Top companies are focusing on AI-driven diagnostics, automation, and diversified test menus to improve accuracy, speed, and accessibility.

What regulatory shifts are redefining this arena?

Rapid approvals of new assays, changing models of reimbursement, and higher quality standards are changing industry compliance.

How is competition intensifying among major players?

Strategic purchases, global growth, and product differentiation through R&D are fueling a more intense competitive landscape.

Which up-and-coming trends will transform point-of-care testing?

Unobtrusive digital integration, pocket next-generation technologies, and expanding use of self-testing options will revolutionize access and effectiveness to diagnostics.

Point of Care Diagnostics Market