Drone Construction Monitoring Market

Drone Construction Monitoring Market Analysis, By Drone Type, By End Use, By Application , and Region - Market Insights 2025 to 2035

Analysis of Drone Construction Monitoring Market Covering 30+ Countries, Including Analysis of US, Canada, UK, Germany, France, Nordics, GCC countries, Japan, Korea and many more

Drone Construction Monitoring Market Outlook (2025 to 2035)

The drone construction monitoring market is valued at USD 414.28 million in 2025. As per Fact.MR analysis, the drone construction monitoring will grow at a CAGR of 13.6% and reach USD 1482.78 million by 2035.

The drone construction monitoring industry experienced a pivotal shift in 2024 as multiple regional contractors and EPC firms moved from pilot-phase drone deployments to full-scale integration. North American homebuilders embraced rotary-wing drones for weekly visual reportage of progress, while commercial construction in Europe required high-definition geospatial mapping to be integrated into BIM.

The infrastructure authorities of Asia favored the use of drones for safety inspection and remote checking to address shortages of skilled manpower. Fact.MR analysis established that 2024 procurement budgets registered a strong trend towards movement away from traditional aerial monitoring and towards autonomous site intelligence systems. [Source: UN Habitat]

The sector begins 2025 with momentum and well-defined avenues for digitalization. Fact.MR research discovered that demand for real-time visual information, automated flight planning, and photogrammetry analytics has become a part of construction processes. The transition has progressed from exploratory to operational.

Drone deployment is at the forefront of minimizing project delays, limiting cost overruns, and maximizing workforce allocation. Site managers are employing drones not merely to monitor progress but also to identify problems pre-emptively, further cementing their strategic value. [Source: World Bank]

Looking ahead, the industry is projected to grow at a CAGR of 13.6% from 2025 to 2035, reaching USD 1,482.78 million. Early movers will benefit from rising mandates for digital project documentation and ESG-aligned transparency in construction workflows, according to Fact.MR analysis.

Drone integration with project management software as well as artificial intelligence-based defect detection will characterize competitive differentiation. Airspace access and UAV weight class regulatory reform will minimize operation bottlenecks worldwide. While clients increasingly insist on quicker, flawless project cycles, drone utilization is transforming from an innovation to an operational imperative. [Source: OECD]

Key Metrics

| Metric | Value |

|---|---|

| Estimated Size in 2025 | USD 414.28 Million |

| Projected Size in 2035 | USD 1482.78 Million |

| CAGR (2025 to 2035) | 13.6% |

Don't Need a Global Report?

save 40%! on Country & Region specific reports

Fact.MR Survey Results: Industry Dynamics Based on Stakeholder Perspectives

(Surveyed Q4 2024, n=500 stakeholder participants evenly distributed across contractors, developers, project managers, and technology providers in the USA, Western Europe, Japan, and South Korea)

Key Priorities of Stakeholders

- Real-Time Data Access & Integration: 85% of stakeholders globally identified real-time data access and integration with project management software as a "critical" priority for efficient project monitoring.

- Compliance with Regulatory Standards: 79% emphasized the importance of complying with local airspace regulations and safety standards, including UAV weight classes and flight zones.

- Automation for Efficiency: 72% of stakeholders prioritized automation of flight paths and data analysis, aiming to minimize human error and improve operational efficiency.

Regional Variance:

- USA: 68% focused on reducing manual reporting through drone automation for tracking project progress.

- Western Europe: 83% emphasized compliance with EU drone regulations and integration of drones into Building Information Modeling (BIM).

- Japan/South Korea: 70% highlighted space optimization for drone operations due to land constraints, favoring compact, foldable drone models.

Adoption of Advanced Technologies

High Variance:

- USA: 60% of construction firms integrated drones with AI-driven defect detection and real-time monitoring to manage large-scale projects.

- Western Europe: 54% employed automated drones with high-resolution sensors for geospatial mapping, particularly for commercial and infrastructure projects.

- Japan: Only 33% adopted advanced drone technologies, citing cost concerns and limited applicability for small projects.

- South Korea: 45% invested in drones with AI-powered analytics for safety audits in urban construction zones.

Convergent and Divergent Perspectives on ROI:

- USA: 72% of stakeholders found drones to be a worthwhile investment, appreciating their role in increasing project transparency and reducing delays.

- Japan/South Korea: Only 40% saw significant ROI, with concerns about over-engineering technology for smaller-scale projects.

Material Preferences

Consensus:

- Carbon Fiber & Lightweight Materials: 58% of global stakeholders favored drones made with lightweight materials like carbon fiber for ease of transport and longer flight durations.

Variance:

- Western Europe: 65% preferred drones with sustainable, recyclable materials, reflecting growing regulatory and consumer demand for eco-friendly solutions.

- USA: 70% selected drones with higher durability (e.g., steel frames) to withstand the rugged conditions of large-scale construction sites.

- Japan/South Korea: 52% preferred compact drones with hybrid materials to balance cost and performance in urban environments.

Price Sensitivity

Shared Challenges:

- Rising Costs of Drone Technology: 82% of stakeholders cited the increasing costs of drones with advanced sensors and AI as a major concern, especially for smaller firms.

Regional Differences:

- USA/Western Europe: 65% were willing to pay a 15-20% premium for drones equipped with automation and AI capabilities.

- Japan/South Korea: 70% preferred lower-cost drone models (under USD 10,000) with minimal advanced features.

- South Korea: 50% expressed interest in leasing drone models to offset upfront costs, compared to 25% in the USA

Pain Points in the Value Chain

Manufacturers:

- USA: 60% faced supply chain disruptions due to the global shortage of semiconductor chips for drone sensors.

- Western Europe: 55% reported challenges in adhering to regulatory requirements for drone certification, especially with evolving airspace policies.

- Japan: 50% dealt with slow adoption rates due to resistance from traditional construction firms that are hesitant to adopt new technology.

Distributors:

- USA: 45% highlighted delays in drone shipments from overseas manufacturers, affecting timely project delivery.

- Western Europe: 40% cited competition from low-cost drone manufacturers in Eastern Europe, threatening margins.

- South Korea: 50% noted logistical issues in distributing drones to remote construction sites.

End-Users (Contractors/Developers):

- USA: 38% highlighted the high initial cost of drones as a barrier despite long-term savings.

- Western Europe: 44% faced difficulties in training workers to operate drones effectively, hindering adoption.

- Japan: 55% cited limited technical support for integrating drones with existing project management systems.

Future Investment Priorities

Alignment:

- 70% of global drone manufacturers plan to invest in R&D to enhance drone autonomy, AI-based defect detection, and real-time data integration capabilities.

Divergence:

- USA: 63% of firms planned to invest in drones equipped with advanced sensor technologies for construction site safety and surveillance.

- Western Europe: 58% focused on enhancing drone capabilities for BIM integration and compliance with sustainability standards.

- Japan/South Korea: 50% targeted compact drone technologies optimized for urban construction environments with limited space for drone operation.

Regulatory Impact

- USA: 75% of stakeholders noted that evolving drone regulations (e.g., FAA's Part 107) were disruptive, adding complexity to operations and delays in project timelines.

- Western Europe: 80% of stakeholders viewed EU airspace regulations (e.g., U-space) as an enabler for more efficient drone deployment, expecting long-term benefits.

- Japan/South Korea: 35% felt that local regulations did not significantly impact their purchasing decisions, citing more relaxed enforcement compared to Western regions.

Conclusion: Variance vs. Consensus

- High Consensus: Key priorities like real-time data integration, automation, and regulatory compliance are global concerns, with stakeholders universally focused on improving operational efficiency.

Key Variances:

- USA: Leading in automation adoption with a strong push for AI and IoT integration.

- Western Europe: Prioritizing sustainability and advanced BIM integration.

- Japan/South Korea: More conservative in adopting expensive, advanced technologies, focusing on cost-effective, space-saving solutions.

Strategic Insight:

A regional approach is critical. The USA should continue advancing automation, while Europe focuses on sustainability and regulatory compliance. In Asia, cost-effective solutions and compact drone models will be key to overcoming adoption barriers.

Impact of Government Regulation

| Country | Impact of Policies & Government Regulations |

|---|---|

| United States |

|

| European Union |

|

| Japan |

|

| South Korea |

|

| China |

|

| Australia |

|

| Canada |

|

| United Kingdom |

|

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

Market Analysis

The industry is set to experience rapid growth, driven by increasing demand for real-time data and automation in project management. As companies embrace drones for enhanced accuracy, cost-efficiency, and compliance with ESG standards, early adopters stand to gain a competitive edge. However, firms slow to integrate these technologies risk falling behind as the industry shifts towards digital, data-driven workflows.

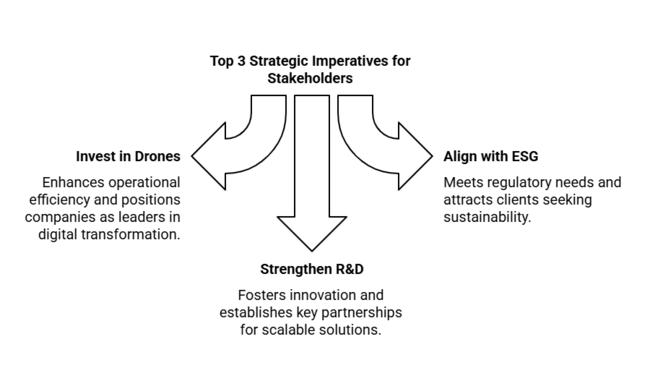

Top 3 Strategic Imperatives for Stakeholders

Invest in Autonomous Drone Integration

To remain competitive, executives must prioritize investment in autonomous drone technology that integrates real-time data collection and AI-driven analytics. This will enhance operational efficiency and position companies as leaders in the digital transformation of construction monitoring.

Align with ESG and Compliance Mandates

Executives should align their strategies with increasing regulatory requirements for ESG compliance and digital documentation. Investing in drones that facilitate accurate reporting and transparency will not only meet regulatory needs but also attract clients demanding sustainability and accountability in their projects.

Strengthen R&D and Strategic Partnerships

Executives must focus on expanding R&D to innovate next-generation drone technologies and establish key partnerships with project management software providers. Strengthening relationships with regulatory bodies and key technology partners will ensure smoother integration, reduce barriers to adoption, and foster scalable solutions across diverse geographies.

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability & Impact |

|---|---|

| Regulatory Delays in Airspace Access- Delays in airspace access regulations could hinder drone deployment and expansion [Source: FAA]. | High Probability, High Impact |

| Technological Limitations in Drone Autonomy- Technical limitations in drone autonomy could affect operational efficiency and scalability [Source: OECD]. | Medium Probability, High Impact |

| Cybersecurity Threats to Data Integrity- Increasing cybersecurity risks could compromise project data integrity, affecting decision-making [Source: World Bank]. | Medium Probability, Medium Impact |

Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Invest in Drone Automation | Run a feasibility study on autonomous drone technology integration for construction monitoring. [Source: OECD] |

| Strengthen Regulatory Compliance | Initiate engagement with regulators on airspace access policies to streamline drone operation approval. [Source: FAA] |

| Cybersecurity Upgrades | Launch a cybersecurity audit for drone data transmission systems to safeguard against increasing threats. [Source: World Bank] |

For the Boardroom

To stay ahead, companies must prioritize investing in autonomous drone technology and strengthen partnerships with regulatory bodies to streamline airspace access. By focusing on real-time data integration and enhancing AI-driven analytics, the client will position themselves as a leader in digital construction workflows. Additionally, bolstering cybersecurity measures will be crucial to safeguard data and mitigate growing risks.

This intelligence shifts the client’s roadmap from adopting drones as an experimental tool to treating them as essential infrastructure for project optimization, compliance, and transparency. Fact.MR analysis found that firms moving quickly to integrate these technologies will be well-positioned to capture industry share as regulatory reforms and client demands drive widespread adoption. [Source: OECD, FAA, World Bank]

Segment-wise Analysis

By Drone Type

Fixed-wing drones are likely to hold a majority of share with their capability to survey large expanses within a single flight, hence perfect for monitoring wide construction areas. They are best suited for procedures like topographic surveys as well as bigger mapping projects. Fixed-wing drones are effective in delivering geospatial information that supports planning, tracking progress, and inspection.

However, their uptake will expand moderately as they require greater takeoff as well as landing spaces and increased costs, limiting their availability to smaller projects. The fixed-wing drone segment will expand at a CAGR of 12.9% to 2035, spurred by large-scale infrastructural projects involving long-range observation.

By End-Use

The construction residential segment will continue to be driven by drone technology through its application in tracking progress, performing site surveys as well as enhancing overall efficiency in residential construction. The growing emphasis on automation and digital integration in construction, coupled with growing demands for quicker, more efficient construction timelines, will spur adoption of drones.

Homebuilders want to automate construction processes, and drones will play a vital role in monitoring the progress of the work and reporting timelines. With the real estate industry expanding, and a growing desire for technology to enhance productivity and save costs, the residential construction segment will witness a CAGR of 14.2% until 2035.

By Application

Site surveying and mapping remain two of the most important applications of drones in construction monitoring. Drones provide high-resolution, accurate data for initial site planning, progress monitoring, and post-construction audits. This usage decreases manual surveys, increasing efficiency as well as safety on site.

Construction projects can move forward more harmoniously with less error and delay by employing drones for these reasons. The demand for precise data is increasing as well as drones can efficiently streamline the planning process. The site mapping and surveying segment is likely to expand at a CAGR of 13.0% by 2035, based on these changing requirements in construction projects.

Country-wise Insights

USA

The USA is likely to register a CAGR of 14.5% between 2025 and 2035. Being one of the biggest industries for construction technology, the USA has seen growing acceptance of drones across residential and commercial construction industries. Demand for accurate mapping and project monitoring has fueled the evolution of construction solutions using drones for construction experts.

Efforts at the federal level such as the Federal Aviation Administration's (FAA) Remote ID regulation and Part 107 rules have streamlined drone operations, making it easier for contractors to implement drone technology in their operations. USA contractors are also using drones more for monitoring progress, safety checks as well as real-time reporting as part of the general smart construction and digitalization movement.

Chief obstacles are regulatory restrictions on drone flight over urban areas and the need for advanced software integration with existing construction management systems. Nevertheless, growing adoption in the private sector and the focus on enhancing construction timelines will guarantee ongoing growth in this industry.

UK

The UK is expected to register a CAGR of 13.2% during 2025 to 2035. The use of drones in the UK construction sector is gaining momentum, especially in the areas of progress monitoring and surveying. With government-backed infrastructure projects and the push for digital construction practices, drone technology has become essential for improving the efficiency of construction projects.

In addition, the UK Civil Aviation Authority (CAA) has established regulations for drone use, providing a clear regulatory framework for operators. The UK's strong commitment to sustainability can be seen in the increased use of drones in gathering high-quality environmental information and improving building practice.

The convergence of drones with Building Information Modeling (BIM) and other construction management technology is likely to gain momentum as construction firms seek to enhance project management and reduce errors. Even though the industry has challenges related to regulatory burden and restrictions on urban flight, the increasing attention to digitizing construction processes will be the major driver.

France

France is projected to register a CAGR of 12.8% during 2025 to 2035. The French government has strict regulations governing the use of drones in the construction industry, with the Directorate General of Civil Aviation (DGAC) holding control. With the maturity of the sector, there is increasing demand for the use of drones to monitor construction sites, conduct topographic surveys, and track project timelines effectively.

The state's investments in infrastructure and efforts at "green" building, i.e., energy-efficient building, are spurring the use of drone technology to track the progress of construction. France's emphasis on sustainable, smart cities is also propelling increased use of digital construction solutions.

Challenges there are to require that drones must follow EU aviation regulations and the cost of incorporating new technology into current workflows. Nevertheless, the increasing demand for data accuracy and the rapid pace of construction in the public sector ensure that the industry will continue to expand in France.

Germany

Germany is anticipated to expand at a CAGR of 13.0% over 2025 to 2035. As Germany focuses on Industry 4.0 and implementing digital building solutions, drones are becoming more valued as critical tools for enhancing site monitoring, safety, and project tracking. The country's high-tech infrastructure projects, including urban renewal and smart city projects, are generating growing demand for drones to supply precise data for Building Information Modeling (BIM).

German regulations are very favorable as well as the European Union Aviation Safety Agency (EASA) has established a standardized pattern for drone usage. Germany also requires robust safety measures and high visibility for drone flights, especially over large construction sites.

As the demand for more efficient, computerized building techniques grows, drones are apt to play an increasingly important role in tracking the activity on sites and providing real-time information to stakeholders. With its innovation obsession and technology-driven solutions, Germany maintains expansion of this sector.

Italy

The projected growth in Italy at the rate of 12.2% from 2025 to 2035 signifies the adoption of drone technology by the construction industry for site monitoring and surveying to reduce project costs and improve data accuracy. The drone industry in Italy has been constituted by a willing attitude of regulations set forth under the European Union aviation regulations, under which a process of some kind of standardization has been laid for the operation of drones in the country.

The sustainable-oriented construction practices and infrastructure development projects in Italy are anticipated to further bolster the demand for construction drones. Italian challenges include disparities in the adoption of construction technology in the different regions, with southern areas falling behind their northern counterparts.

In addition, Italian laws mandate drones to meet both EU-wide and domestic safety standards, which can be time-consuming for the deployment process. However, as Italian construction companies seek to streamline processes and minimize the environmental footprint of their operations, drone use will only expand.

South Korea

South Korea is anticipated to grow at a CAGR of 13.5% from 2025 to 2035. The South Korean government has made substantial investments in smart city projects, and drones are becoming increasingly integrated into construction site management for real-time monitoring, safety inspections, and data collection.

The strict regulations imposed by the Ministry of Land, Infrastructure and Transport of South Korea have effectively legalized drone operation on construction sites. Both well-developed technological infrastructure and keen attention to urbanization drive a strong motive for the use of drones in construction in South Korea.

South Korea is also a geographical and demographic challenge in that it has a small area with high population density. Use of drones for monitoring urban construction projects becomes critical and increasingly integrated. This sector is facing challenges in terms of airspace restrictions and privacy issues and yet the government is moving towards increased incorporation of drones under public infrastructure projects for robust growth.

Japan

Japan is forecast to develop at a CAGR of 12.0% during the period 2025 to 2035. Japan is at the forefront of construction technology innovation, and drones are being increasingly used for site monitoring, topographical surveys, and safety inspections. The industry is also fueled by the aging infrastructure in the country, which requires drones to be used for routine inspection and maintenance.

The Civil Aviation Bureau (CAB) of Japan requires that stated regulations make some permissions necessary to operate drones commercially in urban areas. Although the regulations might be a bit on the restrictive side for mass adoption, Japan's push toward digitization and automation of construction practice in fact creates ample opportunities for growth in the industry.

Moreover, the increasing emphasis on disaster resilience in construction works further fuels demand for drone technologies that can monitor and evaluate project progress in real time.

China

China is forecast to develop at a CAGR of 15.0% during 2025 to 2035. Due to fast infrastructure growth and urbanization, China is a priority industry for drone technology in construction. The government of China initiated a smart city program and moved into an integrated digital construction technology, creating a need for drones to track site activities at construction areas.

While China has an advanced regulatory system, with a need for local permits in addition to compliance with rules of the Civil Aviation Administration of China (CAAC), the sector remains strong because of the emphasis of the government on mass-scale construction work.

The focus of the government on green building codes and smart city infrastructure guarantees continued growth in the use of drones for construction monitoring. Additionally, the combination of drones with AI-based project management software will remain a key driver in China's fast-changing construction sector.

Market Share Analysis

DJI Innovations: 35-40%

DJI will remain industry leader with its extensive hardware offerings and extensive global presence. In 2025, it will launch new drone models with increased flight duration and payload capacity for large-scale construction projects. The company's established industry share will enable it to retain its leading position as the demand for drones in infrastructure projects increases across the world.

Skydio Inc.: 12-15%

Skydio will see rapid growth from its leadership in autonomous drones powered by AI. By 2025, it will target embedding autonomous flight technology in construction sites with real-time data processing and streamlined monitoring. With more construction projects embracing automation, Skydio's cutting-edge AI capabilities will witness increased adoption rates, particularly in dynamic and complex settings.

DroneDeploy:10-12%

DroneDeploy will maintain its expansion through its emphasis on construction analytics software, a space in which it is well established. In 2025, the firm will expand its cloud-based platform to offer even greater precision in data processing and compatibility with BIM technology. With construction firms giving increasing priority to data analytics for site monitoring and planning, DroneDeploy's software will be invaluable in enhancing productivity and project outcomes.

Trimble Inc.: 8-10%

Trimble will have a steady presence via its integration of BIM and construction technology and drones. During 2025, the firm will increase capabilities with the use of drones integrating into advanced construction software for even more efficient project monitoring and management. Its seamless integration between the drones and construction technology currently being used will establish it as the top selection among big infrastructure projects.

Parrot SA: 5-7%

Parrot is also expected to witness steady growth, especially in Europe, with its business drone offerings. In 2025, Parrot will concentrate on building its drone hardware to cater to construction use, especially small- to medium-scale projects. Its focus on affordable and user-friendly solutions will ensure it gets industry traction from small construction companies eager to integrate drones into their business processes.

Kespry: 4-6%

Kespry will go on to enjoy continued growth through specializing in mining and heavy construction. In 2025, the company will release new models of drones targeted at quarry and aggregate industries. With growing demand for drones to be used on large-scale mining and construction projects, Kespry's specialty solutions will be responsible for driving its growth, especially in the USA and other top construction areas.

Other Key Players

- Teledyne Flir LLC (Teledyne Technologies)

- AeroVironment Inc.

- Delair

- Yuneec International Co. Ltd.

- PrecisionHawk Inc.

- Aerialtronics

- 3D Robotics

Drone Construction Monitoring Market Segmentation

By Drone Type:

- Fixed Wing

- Rotary Wing

By End Use:

- Residential Construction

- Commercial Construction

- Industrial Construction

- Infrastructure Projects

By Application:

- Site Surveying and Mapping

- Progress Monitoring

- Safety Inspections

- Equipment Tracking

- Post-Construction Audit

- Others

By Region:

- North America

- Latin America

- Europe

- East Asia

- South Asia & Oceania

- Middle East & Africa

Table of Content

- Global Market - Executive Summary

- Market Overview

- Market Background and Foundation Data (2020 to 2024)

- Global Market - Pricing Analysis (2025 to 2035)

- Global Market Value (USD Million) Analysis and Forecast (2025 to 2035)

- Global Market Analysis and Forecast, By Drone Type (2025 to 2035)

- Fixed Wing

- Rotary Wing

- Global Market Analysis and Forecast, By End Use (2025 to 2035)

- Residential Construction

- Commercial Construction

- Industrial Construction

- Infrastructure Projects

- Global Market Analysis and Forecast, By Application (2025 to 2035)

- Site Surveying and Mapping

- Progress Monitoring

- Safety Inspections

- Equipment Tracking

- Post-Construction Audit

- Others

- Global Market Analysis and Forecast, By Region (2025 to 2035)

- North America

- Latin America

- Europe

- East Asia

- South Asia & Oceania

- Middle East & Africa

- North America Market Analysis and Forecast (2025 to 2035)

- Latin America Market Analysis and Forecast (2025 to 2035)

- Europe Market Analysis and Forecast (2025 to 2035)

- East Asia Market Analysis and Forecast (2025 to 2035)

- South Asia & Oceania Market Analysis and Forecast (2025 to 2035)

- Middle East & Africa Market Analysis and Forecast (2025 to 2035)

- Country-Level Market Analysis and Forecast (2025 to 2035)

- Market Structure Analysis

- Competitive Landscape and Product Launch Analysis

- DJI Innovations

- Trimble Inc.

- Parrot SA

- Skydio Inc.

- Kespry

- DroneDeploy

- Teledyne Flir LLC (Teledyne Technologies)

- AeroVironment Inc.

- Delair

- Yuneec International Co. Ltd.

- PrecisionHawk Inc.

- Aerialtronics

- 3D Robotics

- Assumptions & Acronyms Used

- Research Methodology

Don't Need a Global Report?

save 40%! on Country & Region specific reports

List Of Table

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

List Of Figures

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

- FAQs -

How does drone technology benefit the construction industry?

Drone technology enhances construction by improving efficiency, safety, and accuracy in surveying, monitoring, and inspections.

What are the key applications of drones in construction monitoring?

Drones are used for site surveying, progress monitoring, safety inspections, equipment tracking, and post-construction audits.

What are the different types of drones used in construction monitoring?

The main types are fixed-wing drones for large-scale surveys and rotary-wing drones for detailed site inspections and mapping.

What is driving the growth of drone adoption in construction?

Advancements in automation, demand for cost-efficiency, and the need for better data collection and analysis are driving the adoption.

How is drone technology improving construction project timelines?

Drones streamline surveying, tracking, and reporting processes, helping to reduce delays and ensure faster project completion.

Drone Construction Monitoring Market