Barytes Market

Barytes Market Analysis, By End-User (Oil and Gas Drilling, Chemical, and Other End User), and Region - Market Insights 2025 to 2035

Analysis of Barytes Market Covering 30+ Countries Including Analysis of USA, Canada, UK, Germany, France, Nordics, GCC countries, Japan, Korea, and many more

Barytes Market (2025 to 2035)

The global barytes market will be valued at USD 1.82 billion by 2025. As per Fact.MR analysis, the industry will grow at a CAGR of 3.7% and reach USD 2.62 billion by 2035. In 2024, the industry saw moderate growth, with demand being led mainly by the oil & gas drilling industry, which still dominated product consumption.

Supply chain disruptions, though less severe than in earlier years, continued to be a problem in some regions, especially in North America and Europe, as a result of geopolitical tensions and logistics bottlenecks. The subsequent crude oil price increase in the first half of the year resulted in intensified drilling activity, thus supporting product consumption.

Price volatility was, however, created by inflation pressures and unstable raw material prices, which affected profit margins in major manufacturers. Environmental issues and changes in the regulatory environment governing mining techniques resulted in more emphasis being placed on environmentally friendly products extraction techniques, which affected production strategies.

Looking ahead to 2025, the industry will keep on growing steadily to reach an estimated industry size of around USD 1.82 billion. It will be driven by continuous demand from the oil & gas industry, along with growing usage in the paints & coatings and plastics sectors. Developing nations in Asia-Pacific, specifically China and India, are likely to propel consumption based on growing infrastructure and industrial operations.

Technological improvements in mineral processing will also promote efficiency and environmental protection, creating long-term sustainability. At a projected CAGR of 3.7%, the products industry will experience steady growth up to 2035 at an estimated industry value of USD 2.62 billion.

Key Metrics

| Metrics | Values |

| Industry Size (2025E) | USD 1.82 billion |

| Industry Value (2035F) | USD 2.62 billion |

| Value-based CAGR (2025 to 2035) | 3.7% |

Don't Need a Global Report?

save 40%! on Country & Region specific reports

Fact.MR Survey on Barytes Industry

Fact.MR Stakeholder Survey Outcomes: Stakeholder Insights

(Surveyed Q4 2024, n=500 stakeholder respondents balanced between mining firms, oil & gas organizations, coatings makers, and manufacturing end-users located in North America, Europe, China, and India)

Priorities of Stakeholders

Conformity to Environmental Laws: 79% of the worldwide stakeholders identified conforming to environmental laws as a "crucial" concern, specifically to the extent of environmentally friendly mine operations.

Supply Chain Stability: 72% of them underscored the importance of stable supply chains because of geopolitical risks and supply disruptions.

Regional Variance

North America: 67% focused on secure sourcing and long-term agreements to reduce supply disruptions, versus 45% in Europe.

Europe: 81% pointed to sustainability drivers (low carbon footprint, environmentally friendly processing), versus 52% in North America.

China/India: 64% underscored cost efficiency in product procurement, focusing on price rather than sustainability, versus 28% in Europe.

Use of Advanced Processing Technologies

High Variance

North America: 55% of mining companies embraced advanced beneficiation processes to increase the purity of the product for industrial use.

Europe: 48% of coating manufacturers applied micronized products to achieve better product performance, driven by Germany (58%).

China: Just 26% of producers adopted high-efficiency milling, due to cost factors and oversupply locally.

India: 39% invested in low-waste extraction methods due to mounting regulatory pressure on mining.

Return on Investment (ROI) Views

73% of North American stakeholders found automation in product processing to be "worth the investment," while 36% of Indian firms still used conventional techniques.

Material Choices

Consensus

High-Purity Barytes: Chosen by 68% in total for its adaptability across industries, especially in oil & gas and coatings.

Variance

Europe: 56% opted for low-carbon product varieties (global average: 38%) owing to strict environmental regulations.

China/India: 42% chose mixed products (lower-grade with synthetic fillers) to balance costs and availability.

North America: 72% focused on high-density products for oil drilling, but demand for substitute weighting agents increased in some states.

Price Sensitivity

Shared Challenges

87% mentioned increasing mining and transport costs (fuel up 28%, labor costs up 15%) as primary concerns.

Regional Differences

North America/Europe: 60%

willingness to pay a 10-18% premium for sustainably mined barytes.

China/India: 75% looked for cost-competitive solutions, with only 15% willing to pay premium prices.

India: 48% wanted flexible pricing structures (e.g., bulk discount), versus 20% in North America.

Pain Points in the Value Chain

Producers

North America: 53% faced labor shortages in the refining and logistics functions.

Europe: 47% mentioned complexity in complying with mining permits, as well as environmental limitations.

China: 61% reported saturation as a result of overproduction in their domestic industry.

Distributors

North America: 68% pointed to delayed shipping from overseas suppliers.

Europe: 51% reported price competition from lower-cost Asian producers.

China/India: 60% mentioned inconsistent ore quality due to unregulated suppliers.

End-Users

North America: 42% reported rising costs of processing additives.

Europe: 38% had difficulty meeting stringent product specifications for specialty uses.

China: 55% encountered logistical challenges when procuring from inland mines.

Future Investment Priorities

Alignment

72% of worldwide mining companies intend to invest in energy-efficient products and processing facilities.

Divergence

North America: 60% in cutting-edge refining techniques for oil & gas uses.

Europe: 59% in carbon-free extraction methods.

China/India: 46% in bulk mining expansions to address increasing demand.

Regulatory Impact

North America

66% identified state and federal environmental policies as "highly disruptive" to conventional mining operations.

Europe

80% perceived the EU's Green Deal initiatives as a driver of premium products demand.

China/India

Only 30% believed regulations impacted purchasing decisions, attributing it to weaker enforcement.

High Consensus: Environmental compliance, supply chain stability, and increasing costs are worldwide concerns.

Conclusion: Variance vs. Consensus

Key Variances

North America: Expansion through high-purity and oil-drilling demand vs. China/India: cost-driven procurement.

Europe: Sustainability leadership vs. Asia: Cost-effective processing preference.

Strategic Insight: Regional adaptation (e.g., North American premium barytes, European sustainability of processing, cost-optimized Chinese/Indian mining) is crucial for entry.

Government Regulations on Barytes Industry

| Country | Policies, Regulations, and Mandatory Certifications |

|---|---|

| India | As of February 20, 2025, the Ministry of Mines reclassified products from a minor to a major mineral. This change aims to enhance exploration and scientific mining, especially for critical minerals associated with barytes. Existing leases are extended to 50 years, with a transition period until June 30, 2025 |

| China | Mining rights applicants must submit an application form, proof of qualifications, development plans, environmental impact assessments, and other specified materials. The licensing authorities decide on applications within 40 days. |

| USA | The USA has comprehensive mining regulations focusing on environmental protection, worker safety, and land reclamation. Companies must comply with federal and state laws, including obtaining necessary permits and adhering to environmental standards. |

| UK | The UK enforces strict mining regulations emphasizing environmental sustainability and safety. Companies must secure relevant permits and demonstrate compliance with health, safety, and environmental standards. |

| France | France adheres to the European Union's certification systems for sustainable mining and resource management. Companies must also comply with the EU's due diligence regulations for the responsible sourcing of minerals, such as the EU Conflict Minerals Regulation. |

| Germany | Germany has a robust legal framework for mining operations, focusing on environmental protection, worker health and safety, and sustainable resource management. The Mining Law (Berggesetz) regulates mining activities, and companies are required to undergo environmental impact assessments. Additionally, compliance with the European Union's environmental directives is mandatory. |

| Italy | Italian mining companies must adhere to EU regulations on sustainable mining practices and may need certifications such as the Responsible Sourcing Certification (RSC) and the EU Conflict Minerals Regulation. |

| Japan | Japan follows international standards for ethical sourcing and environmental sustainability. Companies in the mining sector may require certifications like the Responsible Minerals Initiative (RMI) or the ISO 14001 Environmental Management Certification. |

| South Korea | South Korean companies involved in mining are required to adhere to international standards for responsible sourcing and environmental sustainability. This includes certifications such as the Responsible Minerals Initiative (RMI) and compliance with global due diligence requirements. |

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

Market Analysis

The industry is set to see steady growth driven by rising demand from the oil & gas, paints & coatings, and plastics sectors, in addition to tightening mining regulations enforcing sustainable sourcing.

India and China, which have well-regulated mining industries, are likely to gain from formal policies, whereas smaller producers risk being bogged down by the costs of compliance and environmental controls. Firms that obtain responsible sourcing certifications and respond to changing regulations will have a competitive advantage in the global supply chain.

Top 3 Strategic Imperatives for Stakeholders

Achieve Secure Compliant Sustainable Supply Chains

Invest in ethical mining practices, obtain regulatory permits, and acquire certifications such as Responsible Minerals Initiative (RMI) to guarantee adherence to changing environmental and governance requirements.

Leverage High-Growth End-Use Industries

Enhance collaborations with strategic sectors including oil & gas, paints & coatings, and plastics by creating value-added products that are higher in performance and sustainability.

Increase Access Through Strategic Partnerships

Form partnerships with logistics players, regional distributors, and mining companies to maximize supply chains, costs, and reach in emerging industries.

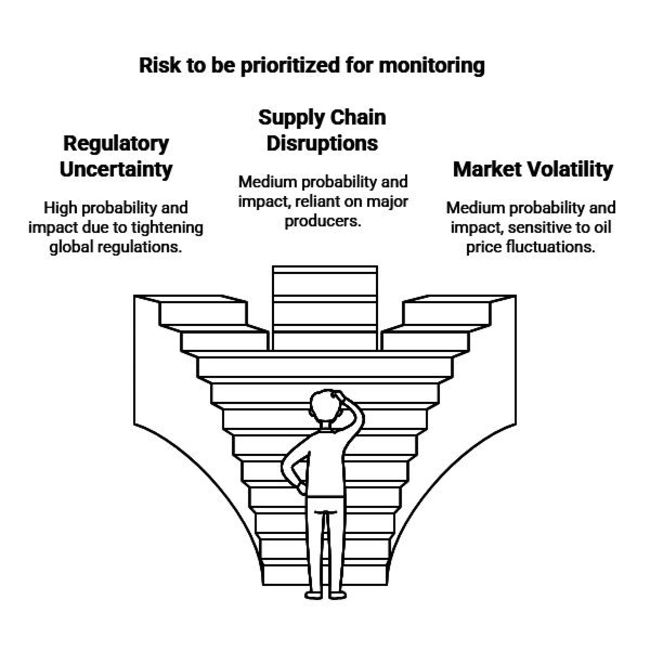

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability/Impact |

|---|---|

| Regulatory Uncertainty and Compliance Costs: Governments worldwide are tightening mining regulations, emphasizing environmental protection, land restoration, and worker safety. Policies such as India’s reclassification of products as a major mineral or China’s strict licensing requirements can raise compliance burdens. | High |

| Supply Chain Disruptions: The supply chain is highly dependent on major producers like China, India, and Morocco. | Medium |

| Volatility in Key End-Use Industries: The oil & gas sector, a major consumer of products in drilling fluids, is highly cyclical and sensitive to crude oil price fluctuations. | Medium |

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Regulatory Adaptation & Compliance | Monitor upcoming policy changes in key players (India, China, USA) and invest in compliance frameworks to mitigate regulatory risks. |

| Supply Chain Resilience | Diversify supplier base and assess feasibility of regional sourcing to reduce dependency on single-country suppliers. |

| Demand & Diversification | Initiate direct engagement with end-users in oil & gas, paints, and plastics to identify emerging needs and potential new applications for barytes. |

For the Boardroom

To stay ahead, companies need to remain ahead in the industry that is changing, Companies must proactively adapt to stringent regulations, establish a robust supply chain, and get in sync with fast-growing end-use sectors.

The action points for the immediate future are enhancing compliance structures, broadening sourcing from conventional suppliers, and intensifying engagement with oil & gas, paints, and plastic manufacturers for innovation.

As ESG pressures intensify, responsible sourcing certifications will not only reduce risks but also unlock premium positioning. This insight changes the roadmap to sustainability-driven growth, strategic partnerships, and supply chain agility-key levers for long-term competitiveness.

Segment-wise Analysis

By End-Users

The oil and gas drilling segment is expected to register 69.1% share in 2025. The oil and gas sector is the biggest user of barytes owing to its vital role as a weighting agent in drilling fluids. The choice is owing to its high specific gravity, chemical inertness, non-corrosiveness, and capacity for controlling formation pressures when used in drilling operations. It prevents blowouts, carries drill cuttings to the surface, minimizes friction, and lubricates the drill bit, making it invaluable in onshore and offshore drilling.

The dependence of the industry on products is also fueled by rising deepwater and shale exploration activities, which need effective drilling mud formulations to increase operational safety and performance. Since global energy demand is still high, petroleum exploration will continue, and this will reinforce barytes' leadership role in this industry.

Country-wise Analysis

USA

The industry in the USAis expected to expand at a CAGR of 4.5% from 2025 to 2035. The USA is a major contributor to the global industry, led mainly by its strong oil and gas sector. The USA is among the world's top producers of oil and natural gas, with widespread drilling operations, especially in areas such as Texas and North Dakota. It is widely utilized as a weighting agent in drilling fluids to manage wellbore pressures and avoid blowouts.

The revival of shale gas production and exploration has also increased the demand for products further. The USA also has a strong chemical industry that employs products in manufacturing barium compounds used in paints, coatings, and plastics. The stringent environmental laws of the country require high-quality products to meet safety and environmental standards.

UK

UK’s sales is affected by its offshore North Sea oil and gas operations. The demand for products in industrial processes and continuous drilling operations will help sustain a modest CAGR of 3.8% during the forecasting period. Even as North Sea output has declined over the years, continuous exploration and decommissioning efforts still demand products for drilling purposes.

It is also used in the UK’s chemical and manufacturing industries to produce paints, coatings, and rubber goods. Yet, the industry is challenged by tough environmental regulations and the move towards alternative sources of energy, which can affect the demand for products in oil and gas usage over the long term.

France

The French sales is mainly boosted by its manufacturing and chemical industries. The industry is anticipated to grow at a CAGR of 3.5% from 2025 to 2035. France has a well-established chemical industry that uses products for the production of barium compounds to be used in paints, coatings, and plastics.

France also utilizes products as a filler substance in rubber and plastic parts in its automotive and aerospace sectors. Though France lacks considerable domestic oil and gas production, industrial applications here offer a consistent demand for products. Green initiatives based on environmental policies might foster the use of products in environmentally friendly applications.

Germany

The industry in Germany enjoys the support of its robust industry base, with a strong presence in the chemical, automotive, and construction industries. The overall German landscape will see a CAGR of 3.7% over the forecast period. The chemical sector applies products in manufacturing barium chemicals, while the automotive industry adds it to brake pads, clutches, and other applications for increased durability and performance.

They find application in high-density concrete radiation shielding in the construction sector. Germany's dedication to environmental stewardship and innovation fuels the evolution of new applications.

Italy

Italy’s sales is underpinned by the country's chemical and industrial bases. The nation uses products for the manufacture of barium chemicals, paint, and coatings. The constant demand from the chemical and construction sectors is expected to continue growing at a CAGR of 3.4% during 2025 to 2035.

The construction sector also uses products in niche applications like radiation-shielding concrete. Italy's oil and gas industry is comparatively smaller, which restricts products usage in drilling purposes. Industry growth can be affected by economic fluctuations and regulation hurdles.

South Korea

The industry in South Korea is spurred by its large chemical and electronics sectors. The chemical industry employs products in barium compound production for a range of applications such as paint, coatings, and plastic. Technological development and industrialization focus by the country promotes a forecasted 4.0% CAGR for the period under consideration.

The electronics sector gains from the advantages of products in the production of radiation-shielding components. South Korea's restricted local products output results in dependency on imports, with the industry being vulnerable to global supply chain fluctuations.

Japan

Japan's industry is shaped by its high-tech manufacturing and chemical sectors. The industry is anticipated to develop at a CAGR of 3.9% between 2025 and 2035, driven by continued industrial uses and advances in technology.

Japan uses products to produce barium chemicals, which are applied in electronics, paint, and plastic. Japan's automotive sector also uses products in brake linings and other parts to improve performance. In spite of a shortage of domestic resources, Japan's focus on high-quality production and technological advancement creates consistent demand.

China

China is the largest producer and user of globally, with much being consumed in its vast oil and gas industry. The industry is expected to grow at a CAGR 5.5% from the forecast. The nation's continuous drilling and exploration operations, especially in areas such as Sichuan and Xinjiang, fuel high demand for products as a drilling weight agent.

The booming manufacturing and construction sectors of China also utilize in plastics, coatings, and paints. The government's emphasis on industrial development and infrastructure building also fuels growth.

Market Share Analysis

Excalibar Minerals LLC

Excalibar Minerals LLC, a subsidiary of Minerals Technologies Inc. (MTI), owns an estimated 15-20% share of the worldwide industry. Excalibar is a leading supplier of API-grade barite to the North American and Middle Eastern oil & gas drilling industries. Its robust logistics infrastructure and stringent quality standards ensure that it is a partner of choice for top drilling companies.

Ashapura Group

Ashapura Group is among India's largest producers, with a 12-18% share. Ashapura has large-scale mining operations in India and exports to the Middle East and Africa, where drilling-grade barite demand is increasing. Ashapura's vertically integrated supply chain and cost-effective production provide it with a competitive advantage in new industries.

Milwhite Inc.

With a 10-15% share, Milwhite Inc. is a key player in North and Latin America. The company specializes in industrial and oilfield-grade barite, supplying drilling mud manufacturers and chemical industries. Its strong distribution network across the Americas ensures steady demand from the oilfield sector.

CIMBAR Performance Minerals

CIMBAR has an 8-12% share in the industry, targeting high-performance barite for industrial use in the USA and Europe. The firm is famous for its ultra-fine barite utilized in coatings, plastics, and adhesives for niche industries requiring high purity.

APMDC (Andhra Pradesh Mineral Development Corporation)

APMDC, a state-owned Indian company, holds a 7-10% share, which is almost entirely supplied by the Mangampet mines (one of the largest deposits in the world). Its Asian-Pacific dominance renders it an important supplier to regional oilfield and chemical industry players.

Sachtleben Minerals GmbH & Co. KG

German company Sachtleben has a share of 5-8% and specializes in high-purity products for coatings, paints, and specialty chemical use. Its dominant position within Europe positions it as the prime supplier of high-value industrial barytes.

Other Key Players

- New Riverside Ochre Company, Inc.

- Deutsche Baryt Industrie

- Spectrum Chemical Manufacturing Corporation

- Anglo Pacific Minerals

- Apmdc

- Seaforth Mineral & Barite Ore Co. Inc

- Other Prominent Players (On Additional Request)

Segmentation

By End-User:

- Oil and Gas Drilling

- Chemical

- Other End Users

By Region:

- North America

- Latin America

- Europe

- East Asia

- South Asia

- Oceania

- Middle East and Africa (MEA)

Table of Content

- Global Market: Executive Summary

- Market Overview

- Market Associated Indicators

- Key Success Factors

- Global Market - Pricing Analysis

- Global Market Value Analysis 2020 to 2024 and Forecast 2025 to 2035

- Global Market Analysis 2020 to 2024 and Forecast 2025 to 2035, By End User

- Oil and Gas Drilling

- Chemical

- Other End User

- Global Market Analysis 2020 to 2024 and Forecast 2025 to 2035, By Region

- North America

- Latin America

- Europe

- Asia Pacific (APAC)

- Middle East and Africa (MEA)

- North America Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- Latin America Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- Europe Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- Asia Pacific (APAC) Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- Middle East and Africa Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- Key Countries Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- Market Structure Analysis

- Competition Analysis

- Milwhite Inc.

- Sachtleben Minerals GmbH & Co. KG

- New Riverside Ochre Company, Inc.

- CIMBAR Performance Minerals

- Deutsche Baryt Industrie

- Spectrum Chemical Manufacturing Corporation

- Anglo Pacific Minerals

- Apmdc

- Ashapura Group

- Seaforth Mineral & Barite Ore Co. Inc

- Excalibar Minerals LLC.

- Other Prominent Players (On Additional Request)

- Assumptions & Acronyms

- Research Methodology

Don't Need a Global Report?

save 40%! on Country & Region specific reports

- FAQs -

What is the projected growth rate of the global barytes market from 2025 to 2035?

The industry is expected to grow at a CAGR of 3.7%, reaching USD 2.62 billion by 2035.

Which industry is the largest consumer of barytes?

The oil & gas industry dominates barytes consumption, accounting for 69.1% of demand in 2025.

Which country will have the highest CAGR in the barytes market?

China is projected to grow at the highest CAGR of 5.5% due to its strong oil, gas, and manufacturing sectors.

What are the key challenges affecting the barytes market?

Supply chain disruptions, price volatility, and stringent environmental regulations pose major challenges.

How is barytes used in industries beyond oil and gas?

It is widely used in paints, coatings, plastics, construction, and high-density concrete for radiation shielding.

Barytes Market