Anticorrosive Primers Market

Anticorrosive Primers Market Analysis by Epoxy-based, Zinc-rich, Pu-based, Alkyd-based, and Acrylic-based for Oil & Gas, Automotive, Marine, Aerospace, Construction, and Others from 2023 to 2033

Analysis of Anticorrosive Primers Market Covering 30+ Countries Including Analysis of US, Canada, UK, Germany, France, Nordics, GCC countries, Japan, Korea and many more

Anticorrosive Primers Market Outlook (2023 to 2033)

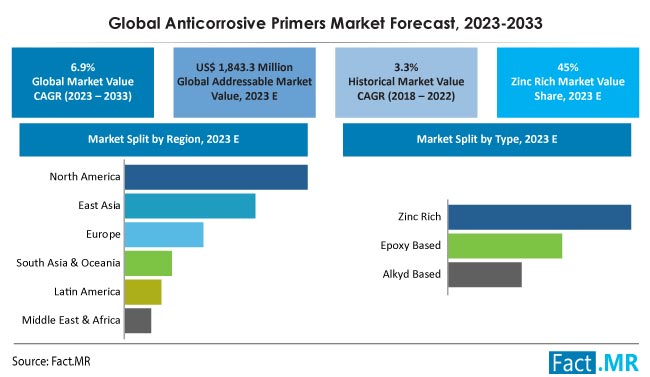

Based on the latest industry analysis by Fact.MR, the global anticorrosive primers market is estimated to be valued at US$ 1.84 billion in 2023 and is forecasted to expand at a CAGR of 6.9% to reach US$ 3.59 billion by the end of 2033.

Anticorrosive primers play an important role in construction projects by preventing the oxidation of metal surfaces. The market has evolved rapidly through technological advancements, ensuring enhanced surface protection from harsh environments, increased use of thin-wall components, and better repair & maintenance of existing structures.

| Report Attributes | Details |

|---|---|

| Anticorrosive Primers Market Size (2022A) | US$ 1.72 Billion |

| Estimated Market Value (2023E) | US$ 1.84 Billion |

| Forecasted Market Value (2033F) | US$ 3.59 Billion |

| Global Market Growth Rate (2023 to 2033) | 6.9% CAGR |

| United States Market Size (2033F) | US$ 1.08 Billion |

| United States Market Growth Rate (2023 to 2033) | 7.4% CAGR |

| Key Companies Profiled | Noroo Paint & Coatings; Peter Kwasny GmbH; Polycote UK; Akzo Nobel; PPG Industries; Sherwin-Williams Company; Jotun Group; Hempel A/s; Rust-Oleum Corporation; Nippon Paints; Kansai Paints; Axalta Coating Systems; Berger Paints India Limited; Asian Paints |

Don't Need a Global Report?

save 40%! on Country & Region specific reports

Consumption Analysis of Anticorrosive Primers (2018 to 2022) vs. Market Projections (2023 to 2033)

Worldwide sales of anticorrosive primers increased at a CAGR of 3.3% from 2018 to 2022. An anticorrosive primer, especially a metal primer, protects metal surfaces from corrosive agents. Evolution of the anticorrosive primers market, driven by technological advancements, has led to their diversified applications across industries.

Demand growth for anticorrosive primers is being influenced by the construction and automotive sectors, as well as the oil & gas, marine, aerospace, power generation, and chemical sectors.

- Short Term (2023 to 2026): Well-established market within the construction and automotive sectors is poised for decent short-term growth, driven by emerging applications. Utilization of anticorrosive primers for welding and providing robust rust protection on exposed metal surfaces is on the rise.

- Medium Term (2026 to 2029): In the medium term, the global market is projected to expand due to technological advancements leading to increasing applications of anticorrosive primers in the power generation sector. The market is anticipated to encompass various uses, including coatings for light, signal, and transmission structures, as well as their incorporation into architectural structures and components.

- Long Term (2029 to 2033): Soaring popularity of anticorrosive primers and continuous expansion of the automotive, aerospace, and construction industries are expected to be the key driving forces behind the long-term growth of the market. Demand for high-quality anticorrosive primers for surface preparation and protection is anticipated to experience a substantial and sustained increase.

The market is predicted to expand at a CAGR of 6.9% during the forecast period (2023 to 2033), according to Fact.MR, a market research and competitive intelligence provider.

Market share analysis of anticorrosive primers based on type and region has been provided in a nutshell in the above image. Under the type segment, zinc-rich anticorrosive primers lead with 45% market share in 2023.

Market Dynamics Outlook

What are the Factors Leading to Increased Adoption of Anticorrosive Primers?

“Extensive Use of Anticorrosive Primers in Automotive Industry”

Demand for anticorrosive primers is on the rise from the manufacturing sector to safeguard equipment from corrosion and ensure durability and luster. Epoxy-based and alkyd-based primers, suitable for traditional steel and galvanized metal surfaces, dominate this usage.

- Global car sales rose from 66.7 million units in 2021 to 67.2 million units in 2022, and are projected to climb further due to increasing demand for electric vehicles driven by sustainability initiatives.

The automotive sector serves as the primary end-user in this market, with epoxy primers essential for corrosion prevention. The expanding automotive industry is set to push the demand for anticorrosive primers.

“Increased Need for Corrosion Protection for Extending Lifespan of Structures & Equipment”

Anticorrosive primers are being used majorly to reduce maintenance costs and improve the quality of structures such as buildings and bridges. Anticorrosive primer coating provides chemical resistance and prevents rust marks on metals due to oxidation.

Growing awareness about the applications of anticorrosive primers by type and end-use industry is driving product demand globally. Anticorrosive primers find extensive applications in the aerospace industry as well.

What Challenges Do Manufacturers of Anticorrosive Primers Encounter?

“Stringent Environmental Regulations Limiting Adoption of Anticorrosive Primers”

Anticorrosive primer producers encounter challenges owing to stringent regulations governing formulations and the volatile organic compounds present in these primers. Such regulations can constrain their application across industries.

The drive for eco-friendly and non-toxic primers is promoting their adoption in diverse sectors. Transitioning from red lead primers to lead- and chromate-free options could mitigate regulatory limitations. Embracing alternative coating solutions, powered by technological progress, offers a pathway to navigate stringent environmental mandates.

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

Country-wise Insights

What’s Driving the Demand Growth for Corrosion Protection Primers in the United States?

“Widespread Use of Anticorrosive Primers in Automotive, Aerospace, and Marine Applications”

The rust prevention primers market in the United States is expected to create an absolute $ opportunity of US$ 552.2 million from 2023 to 2033. The United States automotive sector significantly influences the growth of the market. Zinc phosphate and epoxy-based solutions, known for their robust rust protection, are integral for safeguarding metal parts and surfaces.

Demand for anticorrosive primers is on the rise in the country, driven by the robust automobile industry as well as the aerospace and marine sectors. This demand extends further across diverse industries including construction, oil & gas, chemical, and power generation, contributing to the continuous growth of the market.

Why is China a Lucrative Market for Anticorrosive Primer Manufacturers?

“Increased Vehicle Production Necessitating Extensive Use of Anticorrosive Materials”

Rapid industrialization and urbanization are driving the sales of anticorrosive primers in China. Growing infrastructure sector in China is also acting as a significant factor driving the market for rust prevention primers. These primers are extensively employed as corrosion inhibitors to prevent the spoiling of structures such as buildings and bridges. China stands as a major player in the vehicle market, boasting substantial annual sales and manufacturing output.

- Local vehicle production in China is anticipated to reach 35 million units yearly by 2025, which will drive the market for protective coatings in the long run.

Category-wise Insights

Why are Zinc-rich Primers Preferred by End Users?

“Widespread Use of Zinc-rich Primers for Effective Protection of Steel Surfaces”

Zinc-rich anticorrosive primers occupy 45% share of the global market for rust inhibitors at present. They are extensively used in manufacturing industries as steel primers for the protection of steel surfaces from corrosion. They act as a shield to protect critical equipment from humidity, moisture, and oxidation. They protect the metal by electrical means and provide outstanding corrosion resistance.

Organic zinc-rich primers are widely used in highly corrosive environments in industries such as oil, energy, marine, and construction. Their significant application extends to sectors such as chemical plants, ships, and power plants. Additionally, inorganic zinc-rich primers serve as standalone weather protection coatings.

Why are Anticorrosive Primers Gaining Traction in the Chemical Industry?

“Key Role of Anticorrosive Primers in Ensuring Safety & Reliability of Chemical Piping”

Anticorrosive primers are applied to the interior and exterior surfaces of tanks to protect them from corrosion caused by the stored chemicals. These primers create a barrier that prevents chemicals from coming into direct contact with the metal substrate, reducing the risk of corrosion and maintaining the structural integrity of the equipment.

Anticorrosive primers are applied to pipe surfaces to protect them from the corrosive effects of transported chemicals. This helps prevent leaks, maintain the flow of chemicals, and ensure the safety and reliability of the piping infrastructure. The expanding chemical industry is poised to create lucrative opportunities for anticorrosive primer manufacturers over the forecast period.

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

Key Strategies of Eminent Market Players

Manufacturers are focusing on continuous product innovation and are investing in research & development to introduce new and improved anticorrosive primers. Diversification plays a pivotal role as manufacturers strive to provide anticorrosion treatment products designed for different industries and environments, addressing a wider spectrum of customer needs.

Producers of anticorrosive primers are pursuing geographic expansion, aiming to enter new regions and countries driven by increased recognition of the diverse anticorrosion applications. Additionally, besides new product launches, strategic collaborations with suppliers, distributors, and retailers will play a vital role, enabling extensive product distribution and accessibility.

- In December 2021, Applied Graphene Materials (AGM) introduced a line of anticorrosive primers utilizing its Genable technology. Their Genable epoxy primer combines graphene with a zinc phosphate additive, catering to both urban and industrial use cases.

- Noroo Paint & Coatings, Peter Kwasny GmbH, Polycote UK, Akzo Nobel, PPG Industries, Sherwin-Williams Company, Jotun Group, Hempel A/s, Rust-Oleum Corporation, Nippon Paints, Kansai Paints, Axalta Coating Systems, Berger Paints India Limited, and Asian Paints are leading anticorrosive primer manufacturers.

In its latest industry report, Fact.MR has furnished comprehensive insights into the pricing strategies of prominent anticorrosive primer manufacturers spanning different regions, sales growth trends, production capacities, and upcoming technological advancements.

Segmentation of Anticorrosive Primers Industry Research

-

By Type :

- Epoxy-based

- Zinc-rich

- PU-based

- Alkyd-based

- Acrylic-based

-

By End-use Industry :

- Oil & Gas

- Automotive

- Marine

- Aerospace

- Construction

- Power Generation

- Chemicals

-

By Region :

- North America

- Latin America

- Europe

- East Asia

- South Asia & Oceania

- Middle East & Africa

Table of Content

- 1. Market - Executive Summary

- 2. Market Overview

- 3. Market Background and Foundation Data

- 4. Global Demand (Litres) Analysis and Forecast

- 5. Global Market - Pricing Analysis

- 6. Global Market Value (US$ million) Analysis and Forecast

- 7. Global Market Analysis and Forecast, By Type

- 7.1. Epoxy-based

- 7.2. Zinc-rich

- 7.3. PU-based

- 7.4. Alkyd-based

- 7.5. Acrylic-based

- 8. Global Market Analysis and Forecast, By End-use Industry

- 8.1. Oil & Gas

- 8.2. Automotive

- 8.3. Marine

- 8.4. Aerospace

- 8.5. Construction

- 8.6. Power Generation

- 8.7. Chemicals

- 9. Global Market Analysis and Forecast, By Region

- 9.1. North America

- 9.2. Latin America

- 9.3. Europe

- 9.4. East Asia

- 9.5. South Asia & Oceania

- 9.6. Middle East & Africa

- 10. North America Market Analysis and Forecast

- 11. Latin America Market Analysis and Forecast

- 12. Europe Market Analysis and Forecast

- 13. East Asia Market Analysis and Forecast

- 14. South Asia & Oceania Market Analysis and Forecast

- 15. Middle East & Africa Market Analysis and Forecast

- 16. Country-level Market Analysis and Forecast

- 17. Market Structure Analysis

- 18. Competition Analysis

- 18.1. Noroo Paint & Coatings

- 18.2. Peter Kwasny GmbH

- 18.3. Polycote UK

- 18.4. Akzo Nobel

- 18.5. PPG Industries

- 18.6. Sherwin-Williams Company

- 18.7. Jotun Group

- 18.8. Hempel A/S

- 18.9. Rust-Oleum Corporation

- 18.10. Nippon Paints

- 18.11. Kansai Paints

- 18.12. Axalta Coating Systems

- 18.13. Berger Paints India Limited

- 18.14. Asian Paints

- 18.15. Other Prominent Players

- 19. Assumptions & Acronyms Used

- 20. Research Methodology

Don't Need a Global Report?

save 40%! on Country & Region specific reports

List Of Table

Table 01. Global Market Value (US$ million), by Region, 2018 to 2022

Table 02. Global Market Value (US$ million) and Forecast by Region, 2023 to 2033

Table 03. Global Market Volume (Litres), by Region, 2018 to 2022

Table 04. Global Market Volume (Litres) and Forecast by Region, 2023 to 2033

Table 05. Global Market Value (US$ million), By Type, 2018 to 2022

Table 06. Global Market Value (US$ million) and Forecast By Type, 2023 to 2033

Table 07. Global Market Volume (Litres), By Type, 2018 to 2022

Table 08. Global Market Volume (Litres) and Forecast By Type, 2023 to 2033

Table 09. Global Market Value (US$ million), By End-use Industry, 2018 to 2022

Table 10. Global Market Value (US$ million) and Forecast By End-use Industry, 2023 to 2033

Table 11. Global Market Volume (Litres), By End-use Industry, 2018 to 2022

Table 12. Global Market Volume (Litres) and Forecast By End-use Industry, 2023 to 2033

Table 13. North America Market Value (US$ million), by Country, 2018 to 2022

Table 14. North America Market Value (US$ million) and Forecast by Country, 2023 to 2033

Table 15. North America Market Volume (Litres), by Country, 2018 to 2022

Table 16. North America Market Volume (Litres) and Forecast by Country, 2023 to 2033

Table 17. North America Market Value (US$ million), By Type, 2018 to 2022

Table 18. North America Market Value (US$ million) and Forecast By Type, 2023 to 2033

Table 19. North America Market Volume (Litres), By Type, 2018 to 2022

Table 20. North America Market Volume (Litres) and Forecast By Type, 2023 to 2033

Table 21. North America Market Value (US$ million), By End-use Industry, 2018 to 2022

Table 22. North America Market Value (US$ million) and Forecast By End-use Industry, 2023 to 2033

Table 23. North America Market Volume (Litres), By End-use Industry, 2018 to 2022

Table 24. North America Market Volume (Litres) and Forecast By End-use Industry, 2023 to 2033

Table 25. Latin America Market Value (US$ million), by Country, 2018 to 2022

Table 26. Latin America Market Value (US$ million) and Forecast by Country, 2023 to 2033

Table 27. Latin America Market Volume (Litres), by Country, 2018 to 2022

Table 28. Latin America Market Volume (Litres) and Forecast by Country, 2023 to 2033

Table 29. Latin America Market Value (US$ million), By Type, 2018 to 2022

Table 30. Latin America Market Value (US$ million) and Forecast By Type, 2023 to 2033

Table 31. Latin America Market Volume (Litres), By Type, 2018 to 2022

Table 32. Latin America Market Volume (Litres) and Forecast By Type, 2023 to 2033

Table 33. Latin America Market Value (US$ million), By End-use Industry, 2018 to 2022

Table 34. Latin America Market Value (US$ million) and Forecast By End-use Industry, 2023 to 2033

Table 35. Latin America Market Volume (Litres), By End-use Industry, 2018 to 2022

Table 36. Latin America Market Volume (Litres) and Forecast By End-use Industry, 2023 to 2033

Table 37. Europe Market Value (US$ million), by Country, 2018 to 2022

Table 38. Europe Market Value (US$ million) and Forecast by Country, 2023 to 2033

Table 39. Europe Market Volume (Litres), by Country, 2018 to 2022

Table 40. Europe Market Volume (Litres) and Forecast by Country, 2023 to 2033

Table 41. Europe Market Value (US$ million), By Type, 2018 to 2022

Table 42. Europe Market Value (US$ million) and Forecast By Type, 2023 to 2033

Table 43. Europe Market Volume (Litres), By Type, 2018 to 2022

Table 44. Europe Market Volume (Litres) and Forecast By Type, 2023 to 2033

Table 45. Europe Market Value (US$ million), By End-use Industry, 2018 to 2022

Table 46. Europe Market Value (US$ million) and Forecast By End-use Industry, 2023 to 2033

Table 47. Europe Market Volume (Litres), By End-use Industry, 2018 to 2022

Table 48. Europe Market Volume (Litres) and Forecast By End-use Industry, 2023 to 2033

Table 49. East Asia Market Value (US$ million), by Country, 2018 to 2022

Table 50. East Asia Market Value (US$ million) and Forecast by Country, 2023 to 2033

Table 51. East Asia Market Volume (Litres), by Country, 2018 to 2022

Table 52. East Asia Market Volume (Litres) and Forecast by Country, 2023 to 2033

Table 53. East Asia Market Value (US$ million), By Type, 2018 to 2022

Table 54. East Asia Market Value (US$ million) and Forecast By Type, 2023 to 2033

Table 55. East Asia Market Volume (Litres), By Type, 2018 to 2022

Table 56. East Asia Market Volume (Litres) and Forecast By Type, 2023 to 2033

Table 57. East Asia Market Value (US$ million), By End-use Industry, 2018 to 2022

Table 58. East Asia Market Value (US$ million) and Forecast By End-use Industry, 2023 to 2033

Table 59. East Asia Market Volume (Litres), By End-use Industry, 2018 to 2022

Table 60. East Asia Market Volume (Litres) and Forecast By End-use Industry, 2023 to 2033

Table 61. South Asia & Oceania Market Value (US$ million), by Country, 2018 to 2022

Table 62. South Asia & Oceania Market Value (US$ million) and Forecast by Country, 2023 to 2033

Table 63. South Asia & Oceania Market Volume (Litres), by Country, 2018 to 2022

Table 64. South Asia & Oceania Market Volume (Litres) and Forecast by Country, 2023 to 2033

Table 65. South Asia & Oceania Market Value (US$ million), By Type, 2018 to 2022

Table 66. South Asia & Oceania Market Value (US$ million) and Forecast By Type, 2023 to 2033

Table 67. South Asia & Oceania Market Volume (Litres), By Type, 2018 to 2022

Table 68. South Asia & Oceania Market Volume (Litres) and Forecast By Type, 2023 to 2033

Table 69. South Asia & Oceania Market Value (US$ million), By End-use Industry, 2018 to 2022

Table 70. South Asia & Oceania Market Value (US$ million) and Forecast By End-use Industry, 2023 to 2033

Table 71. South Asia & Oceania Market Volume (Litres), By End-use Industry, 2018 to 2022

Table 72. South Asia & Oceania Market Volume (Litres) and Forecast By End-use Industry, 2023 to 2033

Table 73. MEA Market Value (US$ million), by Country, 2018 to 2022

Table 74. MEA Market Value (US$ million) and Forecast by Country, 2023 to 2033

Table 75. MEA Market Volume (Litres), by Country, 2018 to 2022

Table 76. MEA Market Volume (Litres) and Forecast by Country, 2023 to 2033

Table 77. MEA Market Value (US$ million), By Type, 2018 to 2022

Table 78. MEA Market Value (US$ million) and Forecast By Type, 2023 to 2033

Table 79. MEA Market Volume (Litres), By Type, 2018 to 2022

Table 80. MEA Market Volume (Litres) and Forecast By Type, 2023 to 2033

Table 81. MEA Market Value (US$ million), By End-use Industry, 2018 to 2022

Table 82. MEA Market Value (US$ million) and Forecast By End-use Industry, 2023 to 2033

Table 83. MEA Market Volume (Litres), By End-use Industry, 2018 to 2022

Table 84. MEA Market Volume (Litres) and Forecast By End-use Industry, 2023 to 2033

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

List Of Figures

Figure 01. Global Market Value (US$ million) and Volume (Litres) Forecast, 2023 to 2033

Figure 02. Global Market Absolute $ Opportunity (US$ million), 2023 to 2033

Figure 03. Global Market Value (US$ million) and Volume (Litres) by Region, 2023 & 2033

Figure 04. Global Market Y-o-Y Growth Rate by Region, 2023 to 2033

Figure 05. Global Market Value (US$ million) and Volume (Litres) By Type, 2023 & 2033

Figure 06. Global Market Y-o-Y Growth Rate By Type, 2023 to 2033

Figure 07. Global Market Value (US$ million) and Volume (Litres) By End-use Industry, 2023 & 2033

Figure 08. Global Market Y-o-Y Growth Rate By End-use Industry, 2023 to 2033

Figure 09. North America Market Value (US$ million) and Volume (Litres) Forecast, 2023 to 2033

Figure 10. North America Market Absolute $ Opportunity (US$ million), 2023 to 2033

Figure 11. North America Market Value (US$ million) and Volume (Litres) by Country, 2023 & 2033

Figure 12. North America Market Y-o-Y Growth Rate by Country, 2023 to 2033

Figure 13. North America Market Value (US$ million) and Volume (Litres) By Type, 2023 & 2033

Figure 14. North America Market Y-o-Y Growth Rate By Type, 2023 to 2033

Figure 15. North America Market Value (US$ million) and Volume (Litres) By End-use Industry, 2023 & 2033

Figure 16. North America Market Y-o-Y Growth Rate By End-use Industry, 2023 to 2033

Figure 17. North America Market Attractiveness Analysis by Country, 2023 to 2033

Figure 18. North America Market Attractiveness Analysis By Type, 2023 to 2033

Figure 19. North America Market Attractiveness Analysis By End-use Industry, 2023 to 2033

Figure 20. Latin America Market Value (US$ million) and Volume (Litres) Forecast, 2023 to 2033

Figure 21. Latin America Market Absolute $ Opportunity (US$ million), 2023 to 2033

Figure 22. Latin America Market Value (US$ million) and Volume (Litres) by Country, 2023 & 2033

Figure 23. Latin America Market Y-o-Y Growth Rate by Country, 2023 to 2033

Figure 24. Latin America Market Value (US$ million) and Volume (Litres) By Type, 2023 & 2033

Figure 25. Latin America Market Y-o-Y Growth Rate By Type, 2023 to 2033

Figure 26. Latin America Market Value (US$ million) and Volume (Litres) By End-use Industry, 2023 & 2033

Figure 27. Latin America Market Y-o-Y Growth Rate By End-use Industry, 2023 to 2033

Figure 28. Latin America Market Attractiveness Analysis by Country, 2023 to 2033

Figure 29. Latin America Market Attractiveness Analysis By Type, 2023 to 2033

Figure 30. Latin America Market Attractiveness Analysis By End-use Industry, 2023 to 2033

Figure 31. Europe Market Value (US$ million) and Volume (Litres) Forecast, 2023 to 2033

Figure 32. Europe Market Absolute $ Opportunity (US$ million), 2023 to 2033

Figure 33. Europe Market Value (US$ million) and Volume (Litres) by Country, 2023 & 2033

Figure 34. Europe Market Y-o-Y Growth Rate by Country, 2023 to 2033

Figure 35. Europe Market Value (US$ million) and Volume (Litres) By Type, 2023 & 2033

Figure 36. Europe Market Y-o-Y Growth Rate By Type, 2023 to 2033

Figure 37. Europe Market Value (US$ million) and Volume (Litres) By End-use Industry, 2023 & 2033

Figure 38. Europe Market Y-o-Y Growth Rate By End-use Industry, 2023 to 2033

Figure 39. Europe Market Attractiveness Analysis by Country, 2023 to 2033

Figure 40. Europe Market Attractiveness Analysis By Type, 2023 to 2033

Figure 41. Europe Market Attractiveness Analysis By End-use Industry, 2023 to 2033

Figure 42. East Asia Market Value (US$ million) and Volume (Litres) Forecast, 2023 to 2033

Figure 43. East Asia Market Absolute $ Opportunity (US$ million), 2023 to 2033

Figure 44. East Asia Market Value (US$ million) and Volume (Litres) by Country, 2023 & 2033

Figure 45. East Asia Market Y-o-Y Growth Rate by Country, 2023 to 2033

Figure 46. East Asia Market Value (US$ million) and Volume (Litres) By Type, 2023 & 2033

Figure 47. East Asia Market Y-o-Y Growth Rate By Type, 2023 to 2033

Figure 48. East Asia Market Value (US$ million) and Volume (Litres) By End-use Industry, 2023 & 2033

Figure 49. East Asia Market Y-o-Y Growth Rate By End-use Industry, 2023 to 2033

Figure 50. East Asia Market Attractiveness Analysis by Country, 2023 to 2033

Figure 51. East Asia Market Attractiveness Analysis By Type, 2023 to 2033

Figure 52. East Asia Market Attractiveness Analysis By End-use Industry, 2023 to 2033

Figure 53. South Asia & Oceania Market Value (US$ million) and Volume (Litres) Forecast, 2023 to 2033

Figure 54. South Asia & Oceania Market Absolute $ Opportunity (US$ million), 2023 to 2033

Figure 55. South Asia & Oceania Market Value (US$ million) and Volume (Litres) by Country, 2023 & 2033

Figure 56. South Asia & Oceania Market Y-o-Y Growth Rate by Country, 2023 to 2033

Figure 57. South Asia & Oceania Market Value (US$ million) and Volume (Litres) By Type, 2023 & 2033

Figure 58. South Asia & Oceania Market Y-o-Y Growth Rate By Type, 2023 to 2033

Figure 59. South Asia & Oceania Market Value (US$ million) and Volume (Litres) By End-use Industry, 2023 & 2033

Figure 60. South Asia & Oceania Market Y-o-Y Growth Rate By End-use Industry, 2023 to 2033

Figure 61. South Asia & Oceania Market Attractiveness Analysis by Country, 2023 to 2033

Figure 62. South Asia & Oceania Market Attractiveness Analysis By Type, 2023 to 2033

Figure 63. South Asia & Oceania Market Attractiveness Analysis By End-use Industry, 2023 to 2033

Figure 64. MEA Market Value (US$ million) and Volume (Litres) Forecast, 2023 to 2033

Figure 65. MEA Market Absolute $ Opportunity (US$ million), 2023 to 2033

Figure 66. MEA Market Value (US$ million) and Volume (Litres) by Country, 2023 & 2033

Figure 67. MEA Market Y-o-Y Growth Rate by Country, 2023 to 2033

Figure 68. MEA Market Value (US$ million) and Volume (Litres) By Type, 2023 & 2033

Figure 69. MEA Market Y-o-Y Growth Rate By Type, 2023 to 2033

Figure 70. MEA Market Value (US$ million) and Volume (Litres) By End-use Industry, 2023 & 2033

Figure 71. MEA Market Y-o-Y Growth Rate By End-use Industry, 2023 to 2033

Figure 72. MEA Market Attractiveness Analysis by Country, 2023 to 2033

Figure 73. MEA Market Attractiveness Analysis By Type, 2023 to 2033

Figure 74. MEA Market Attractiveness Analysis By End-use Industry, 2023 to 2033

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

- FAQs -

What was the size of the anticorrosive primers market in 2022?

The global anticorrosive primers market was valued at US$ 1.72 billion in 2022.

At what rate did the sales of anticorrosive primers increase from 2018 to 2022?

Worldwide sales of anticorrosive primers increased at 3.3% CAGR from 2018 to 2022.

Which regions have been included in the market study on anticorrosive primers?

North America, Latin America, South Asia & Oceania, East Asia, Europe, and MEA are included in this study.

Who are the leading manufacturers of anticorrosive primers?

Prominent players in the market are Noroo Paint & Coatings, Polycote UK, Akzo Nobel, and Asian Paints.

What is the estimated valuation of the global market for 2033?

The market for anticorrosive primers is expected to reach US$ 1.84 billion in 2033.

What are the sales projection for anticorrosive primers in the United States?

Sales of anticorrosive primers in the U.S. are set to reach US$ 1.08 billion by 2033.

What is the estimated valuation of the market in China for 2033?

The market in China is expected to reach US$ 571.2 million by 2033.

Anticorrosive Primers Market