Flame Retardant Coating Additives Market

Flame Retardant Coating Additives Industry Analysis by Type, End-Use, and Region through 2035

Analysis of Flame Retardant Coating Additives Market Covering 30+ Countries Including Analysis of US, Canada, UK, Germany, France, Nordics, GCC countries, Japan, Korea and many more

Flame Retardant Coating Additives Market Outlook (2025 to 2035)

The flame retardant coating additives market will be valued at USD 10.18 billion by 2025 end. As per Fact.MR's analysis, flame retardant coating additives will grow at a CAGR of 7.1% and reach USD 19.61 billion by 2035.

In 2024, the industry for flame retardants continued to expand as sectors such as electrical & electronics, construction, and transportation increasingly used fire-resistant products to address changing safety standards.

The major drivers were strict laws and increased fire safety consciousness among consumers. Certain industries, such as the construction sector, experienced growth in fire-resistant insulation materials, while the demand for electrical components with increased fire resistance skyrocketed following higher consumption of electrical goods.

From 2025 and beyond, flame retardant demand is anticipated to keep expanding as a result of increasing regulations, advances in fire-resistant materials technology, and continued movement toward sustainable and efficient flame retardants across industries.

The worldwide movement toward greater fire safety will probably generate additional innovation and use of flame retardants, especially in the developing world.

Key Metrics

| Metrics | Values |

|---|---|

| Industry Size (2025E) | USD 10.18 billion |

| Industry Value (2035F) | USD 19.61 billion |

| Value-based CAGR (2025 to 2035) | 7.1% |

Don't Need a Global Report?

save 40%! on Country & Region specific reports

Fact.MR Survey on Flame Retardant Coating Additives Industry

Fact.MR Survey Findings: Trends According to Stakeholder Insights

(Surveyed Q4 2024, n=500 stakeholder respondents evenly split between manufacturers, distributors, and end-users in the US, Western Europe, Japan, and South Korea)

Priorities of Stakeholders

- Fire Safety Regulation Compliance: 80% cited fire safety compliance as a "critical" priority.

- Durability and Performance: 75% highlighted the requirement for long-lasting, high-performance additives for industrial and construction uses.

Regional Variance:

- US: 65% stressed sustainability (low-toxicity, environmentally friendly formulations), as against 50% in Japan.

- Western Europe: 70% stressed innovation in water-based flame retardants for construction uses, against 40% in the US.

- Japan/South Korea: 55% stressed adhering to stringent local fire safety regulations.

Use of Advanced Technologies

- US: 60% of the stakeholders used flame retardants with built-in smart technology (e.g., temperature sensors), primarily in construction.

- Western Europe: 50% had an interest in developing bio-based flame retardants because of sustainability issues.

- Japan/South Korea: 45% applied emerging technologies to enhance coating efficiency for auto and electronics industries.

Material Preferences

- Consensus: 68% had phosphorus-based additives due to high efficacy.

Regional Variations:

- Western Europe: 60% had silicon-based coatings because of environmental norms.

- US: 55% had bromine-based additives for industrial use owing to preference.

Price Sensitivity

- Global Challenge: 85% mentioned rising raw material prices (phosphorus, bromine) as an important issue.

Regional Differences:

- US/Western Europe: 50% were willing to pay a 10-15% premium for high-performance, environmentally friendly flame retardants.

- Japan/South Korea: 72% were willing to settle for cost-efficient additives to retain competitive pricing for electronics.

Pain Points in the Value Chain

Manufacturers:

- US: 50% had to deal with volatile raw material prices.

- Western Europe: 40% had trouble ensuring compliance with strict EU legislation.

Distributors:

- US: 45% encountered logistics interruptions, especially when importing specialty chemicals.

- South Korea: 60% experienced trade restrictions-caused delays in supply chains within their region.

End-Users:

- US: 50% complained about difficulty implementing new flame retardant technologies on existing systems.

Investment Priorities of the Future

- Alignment: 70% of international manufacturers are investing in future-generation eco-flame retardants.

Divergence:

- US: 55% concentrated on R&D high-performance coatings for construction.

- Western Europe: 60% targeted green certifications of flame retardants.

- Japan/South Korea: 50% expressed target advanced technologies to lower environmental impact.

Regulatory Impact

- US: 60% saw changing fire safety regulations (e.g., California's stricter codes) as a growth driver.

- Western Europe: 75% favored sustainable flame retardant-oriented regulations.

- Japan/South Korea: 40% cited regulatory impact but slower implementation of standards.

Conclusion

- High Consensus: Standard compliance and lifespan are primary worldwide priorities.

Key Variances:

- US: High-performance and innovation-centered.

- Western Europe: Preference influenced by sustainability.

- Asia: Emphasis on cost-efficient, region-specific solutions.

Strategic Insight:

Region-specific strategies, with environmentally friendly formulations given priority in Europe and high-performance solutions in the US.

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

Government Regulations on Flame Retardant Coating Additives Industry

| Country | Impact of Policies/Regulations |

|---|---|

| U.S. | California Proposition 65: Requires labeling for products with flame retardants if they contain harmful chemicals. TSCA (Toxic Substances Control Act): Regulations on chemicals used in flame retardants. NFPA Standards: Fire safety regulations in construction and industry sectors |

| European Union | REACH Regulation: This governs chemical use, including flame retardants. RoHS Directive: Limits hazardous substances in electrical equipment, affecting flame retardants used in electronics. EU Fire Safety Regulations: Require flame-retardant treatments in building materials. |

| Japan | Chemical Substances Control Law (CSCL): Monitors chemicals used in products, including flame retardants. Fire Services Act: Regulates fire safety standards for materials, influencing the use of flame retardants in construction. |

| South Korea | K-REACH (Korea Toxic Chemicals Control Act): Regulates the production and sale of flame retardants. KFS (Korea Fire Safety Act): Mandates fire-resistant materials in buildings, influencing the demand for flame retardants. |

Market Analysis

The industry is fueled by heightened fire safety regulations, especially in the construction and electronics industries. Businesses focusing on environmentally friendly, high-performance products are best placed for expansion, while those using conventional, less-regulated products could be threatened. With tightening environmental standards, manufacturers will gain from improved, sustainable, high-efficiency flame retardants, while those behind the times could lose industry share.

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

Top 3 Strategic Imperatives for Stakeholders

Invest in Green Flame Retardants

Executives should focus on developing and selling environment-friendly, low-toxicity flame retardants to address the mounting global demand for sustainable products. This will get their products ready for future legislation.

Align with Fire Safety Regulations

Emphasize products that are compliant with high fire safety standards in various geographies, especially in construction and electronics, where regulatory intensity is greatest.

Enhance Partnerships and R&D

Invest in R&D of next-generation flame retardants while making strategic partnerships with construction and electronics firms to boost product integration and stimulate uptake.

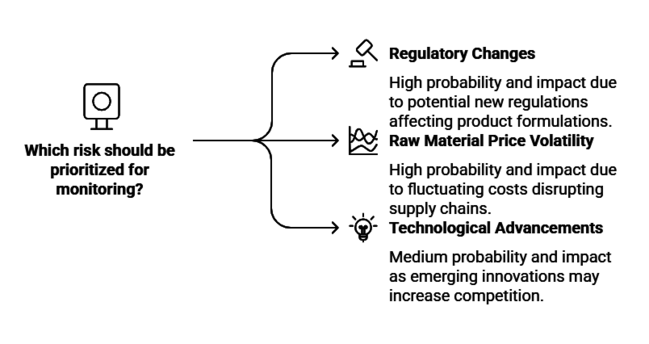

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability/Impact |

|---|---|

| Regulatory Changes - New, stricter fire safety and environmental regulations could emerge, impacting product formulations. | High |

| Raw Material Price Volatility - Fluctuations in the cost of key chemicals like phosphorus and bromine can disrupt supply chains. | High |

| Technological Advancements by Competitors - Emerging innovations in flame retardants may lead to increased competition. | Medium |

Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Sustainability Focus | Run a feasibility study on eco-friendly flame retardants and their demand. |

| Regulatory Compliance | Initiate analysis of upcoming fire safety regulations in key regions (US, EU, Asia). |

| Technological Advancements | Explore partnerships for R&D in next-gen flame retardant technologies. |

For the Boardroom

To stay ahead and remain competitive in the changing flame retardant coatings industry, the firm needs to focus on investment in sustainable and environmentally friendly products in order to comply with increasingly stringent global regulations.

R&D of next-generation products that meet environmental and fire safety requirements should be the priority at hand. Fostering greater collaboration with regulatory agencies and customers will be instrumental in ensuring smooth penetration.

This intelligence redirects the roadmap towards quicker cycles of innovation, regulatory foresight, and strategic partnerships, making the company not only compliant but also leading in sustainability.

Segment-wise Analysis

By Type

Among the enumerated flame retardant additives, antimony oxide is used most extensively because of its high synergy with brominated flame retardants.

It catalyzes the properties of flame retardancy, enhancing the fire resistance and general performance of products such as plastics and textiles.

It is especially popular in industries such as electronics and automotive, where efficiency and high performance are paramount. This broad application is spurred by its efficiency and comparatively cost-effective operation as compared to other options.

In addition, antimony oxide has superior thermal stability and hardness, which guarantees long-term fire retardation in industrial as well as consumer usage.

Its versatility and compatibility with various polymer systems make it one of the best-selling flame retardant additives in the market.

By End-Use

The Building and Construction industry is the biggest consumer of flame retardant coatings because of strict fire safety standards, particularly following high-profile fires. Flame retardants play a crucial role in safeguarding structural material, insulation, and cladding against fire risk, providing safety and regulatory compliance.

The current construction boom worldwide, combined with more stringent building regulations, stimulates steady demand for flame retardant solutions in this sector, and it is the most important application area versus others such as aerospace or automotive.

Moreover, commercial buildings, tunnels, and high-rise buildings need sophisticated fire-resistant solutions to reduce risks from fire hazards. The increasing focus on sustainable and eco-friendly building materials has also spurred developments in halogen-free and low-toxicity flame retardant additives.

Country-wise Analysis

| Countries | CAGR |

|---|---|

| U.S. | 7.5% |

| UK | 6.8% |

| France | 6.2% |

| Germany | 7.2% |

| Italy | 5.9% |

| South Korea | 6.0% |

| Japan | 5.5% |

| China | 8.0% |

U.S.

Sales in the United States will witness a high CAGR of 7.5% in the industry for flame retardant coatings from 2025 to 2035. The growth results from the strict fire safety norms in industries like construction, automotive, and electronics.

Product codes like National Fire Protection Association (NFPA) codes and state codes like California's Proposition 65 are propelling demand towards higher levels of flame retardants in products, mainly in building construction materials and home electronics. Growing fire awareness, especially among higher-risk markets such as commercial buildings and high-rises, is also driving demand.

The U.S. also has high uptake of new technologies like IoT-based flame retardant solutions in electrical equipment. However, challenges such as rising material costs and regulatory problems may temper growth by a notch. Either way, innovation in green and non-toxic flame retardants will likely create new opportunities and position the U.S. as a world leader.

UK

Market in the United Kingdom is also expected to record a CAGR of 6.8% over the period 2025 to 2035 in flame retardant coatings. The sector is led most by escalating fire safety regulation, particularly within the construction industry, following massive accidents like the Grenfell Tower fire.

The UK's focus on reducing carbon emissions further grows demand for cleaner flame retardant products, with the nation focusing on green building strategies. The use of fire-resistant materials in public structures, residential structures, and infrastructure construction is anticipated to drive growth.

Along with this, the UK industry is obeying European Union regulations even after Brexit, particularly fire safety standards that are still affecting building codes. The automotive sector, particularly electric vehicle production, is also driving the growing demand for flame retardant coatings. Manufacturers are trying to develop environmentally friendly and halogen-free flame retardants to address the sustainability goals of the UK government.

France

Market in the flame retardant coatings market in France is projected to increase at a CAGR of 6.2% during 2025 to 2035. The market is dominated by the strong regulatory environment for fire protection, primarily in the construction and transport sectors.

France also has stringent fire safety laws, particularly in the public domain, such as enormous office buildings, business centers, and multi-story apartments, where the application of fire-resistance materials is mandatory.

Government sustainability efforts are also fueling demand for environmentally friendly flame retardant solutions with a big push to reduce the environmental impacts of chemicals used in building and automotive production industries.

Rise in application of fire-resistant coating in electric vehicles and renewable systems is still driving demand for newer generation flame retardants. Also, France is seeing more investment in infrastructure programs, still fueling demand for fire-resistant items. However, an increase in the cost of raw materials like phosphorus and bromine might slow growth if companies are unable to absorb the additional cost.

Germany

Germany is expected to grow at a CAGR of 7.2% over the 2025 to 2035 period in the market for flame retardant coatings. Germany’s strict fire protection rules, particularly in construction and automobiles, are the prime drivers of demand for flame retardant products.

Demand for sustainable flame retardants is gaining acceptance more and more both because of pressures from regulators as well as from consumers' preference for greener products. In addition to construction, the automotive industry, specifically the growing electric vehicle market, is also stimulating demand for flame retardants.

Germany's dominance in industrial automation and technology also demands cutting-edge fireproof materials in electronics and electrical parts. The strong manufacturing sector of the country, including the manufacturing of building products, also offers tremendous growth opportunities for the flame retardant coatings industry.

Although the industry is increasing, issues regarding raw material costs, environmental protection, and stringent regulation of chemicals continue to be main obstacles for manufacturers to overcome.

Italy

The flame retardant coatings industry in Italy is predicted to increase at a CAGR of 5.9% between 2025 and 2035. The primary driving force for the expansion is the country's evolving fire safety regulations, particularly in the construction industry.

The increasing focus on fire-resistant building materials, domestic and European Union fire codes, is driving the application of flame retardants. The retrofitting of existing buildings with fire-resistant coatings also fuels expansion.

Further, Italy's robust automotive and aerospace sectors, needing flame-resistant coatings for safety and functionality, will sustain demand for these products.

The increased need for cleaner, non-toxic flame retardants in these industries, in combination with a governmental push toward sustainability, also opens the door to innovation opportunities by manufacturers filling the industry gap.

Italy's delayed use of advanced high-tech flame retardants behind other parts of Europe will reduce growth opportunity over the next short period.

South Korea

South Korea's flame retardant coatings industry is projected to expand at a CAGR of 6.0% during the 2025 to 2035 forecast period. South Korea is experiencing growing demand for flame retardant solutions owing to stringent fire safety regulations, especially in the construction and electronics industries.

The urbanization and high-density living environments in the country have fueled the demand for fire-resistant materials in residential and commercial buildings.

In addition, South Korea's electronics industry, like manufacturing smartphones, TVs, and other electronic items, requires flame retardant coatings to satisfy safety standards. The automotive sector, particularly electric vehicles, also contributes to increasing the demand for flame retardants. The challenge, however, lies in finding the correct balance between cost-effective solutions and mounting regulatory pressure for higher performance and environmentally friendly solutions.

Japan

Japan's flame retardant coatings market will advance at a CAGR of 5.5% during 2025 to 2035. Japan's strict fire protection regulations, especially in the construction and electronics sectors, will continue to drive demand for flame retardants. The country is known for its advanced technology and is increasingly adopting IoT-based flame retardant solutions, particularly in electrical and electronic devices.

Japan is also focusing on sustainability, with the government promoting green construction methods, which will drive demand for non-toxic flame retardant solutions. The automotive sector, particularly due to Japan's strong focus on electric vehicle production, will require flame retardants due to safety considerations. While all these opportunities are present, Japan's growth will be sluggish compared to other countries due to its conservative inclination towards new technologies and the cost factor as a result of using advanced flame retardant formulations.

China

China is expected to have the highest CAGR of 8.0% in the flame retardant coatings market over 2025 to 2035. The country's rapidly growing construction, automotive, and electronics sectors will continue to drive the demand for flame retardant materials. China's massive infrastructure projects and urbanization initiatives are some of the main drivers of the increased demand for fire-resistant products.

In addition, China's increasing electric vehicle industry is pushing enhanced fire protection regulations, adding further to the use of flame retardants. Increased Chinese government focus on environmental governance, including chemical use and sustainability, is driving green, non-toxic flame retardant production and application.

Market Share Analysis

BASF SE is set to consolidate its leadership with a forecasted 19-21% share by 2025. The German chemical giant is building its portfolio of halogen-free intumescent coatings specifically for the protection of electric vehicle batteries while, at the same time, introducing new bio-based flame retardant formulations to meet the stringent environmental requirements of the EU Green Deal. BASF is securing its position with strategic partnerships with original automotive equipment manufacturers to create fire-resistant lightweight materials, especially for the expanding EV industry in North America and Europe.

Dow Chemical Company plans to increase its share to 16-18% by 2025. The US-based multinational is riding strong demand for its reactive flame retardants used in next-generation 5G infrastructure and data center deployments. Dow is heavily investing in circular economy offerings, such as novel flame retardants with recycled content. The company is witnessing particularly robust sales growth in Asia-Pacific economies as China's red-hot construction and electronics industries drive heavy demand for high-performance coating additives.

Lanxess AG is expected to hold 13-15% of the shares by 2025. The specialty chemicals firm is witnessing a growing uptake of its phosphorus-based additives in advanced electric vehicle and aerospace technologies. Adapting to regulatory shifts, Lanxess is rapidly developing its bromine-free product ranges in the European lanscape. The strategic acquisition of Emerald Kalama Chemical by the company in 2024 has greatly strengthened its specialty additives portfolio, setting it up for more robust growth in niche industries.

Clariant AG hopes to increase its share to 11-13% by 2025. The Swiss specialty chemicals company is riding strong demand for its environmentally friendly synergist systems, especially in sustainable construction applications. Clariant is leading the development of nanotechnology-based flame retardants that deliver enhanced performance in thin-film coatings. Clariant has managed to build on its North American presence after consolidating acquired BASF flame retardant assets, further solidifying its position in major industrial industries.

AkzoNobel N.V. predicts achieving 9-11% market share by the year 2025. The leading Dutch coatings company has launched the latest generation of intumescent coatings that are designed specifically for the protection of offshore wind energy infrastructure. Strategic partnerships with leading European construction companies have been established by AkzoNobel to provide superior fire-safe architectural coatings. AkzoNobel is also growing at a record rate in the Middle Eastern and African economies, where its advanced fireproofing products for oil and gas segments are creating huge demand.

Key Players

- Albemarle

- BASF

- Clariant

- DuPont

- ICL

- Italmatch

- Lanxess

- Nabaltec

Segmentation

By Type :

With respect to the type, it is classified into ATH, antimony oxide, brominated, chlorinated, phosphorous, zinc sulfide, zinc oxide, boron compounds, and others.

By End-Use :

In terms of end-use, it is divided into aerospace, automotive and transportation, building and construction, electronics and appliances, furniture, and others.

By Region :

In terms of region, it is segmented into North America, Latin America, Europe, East Asia, South Asia, Oceania, and MEA.

Table of Content

- 1. Executive Summary

- 2. Market Overview

- 3. Key Market Trends

- 4. Market Background

- 5. Global Market Demand Analysis 2020 to 2024 and Forecast 2025 to 2035

- 6. Global Market - Pricing Analysis

- 7. Global Market Demand (US$ Mn) Analysis 2020 to 2024 and Forecast 2025 to 2035

- 8. Global Market Analysis 2020 to 2024 and Forecast 2025 to 2035 By Type

- 8.1. ATH

- 8.2. Antimony Oxide

- 8.3. Brominated

- 8.4. Chlorinated

- 8.5. Phosphorous

- 8.6. Zinc Sulfide

- 8.7. Zinc Oxide

- 8.8. Boron Compounds

- 8.9. Others

- 9. Global Market Analysis 2020 to 2024 and Forecast 2025 to 2035, By End-use

- 9.1. Aerospace

- 9.2. Automotive and Transportation

- 9.3. Building and Construction

- 9.4. Electronics and Appliances

- 9.5. Furniture

- 9.6. Others

- 10. Global Market Analysis 2020 to 2024 and Forecast 2025 to 2035 by Region

- 10.1. North America

- 10.2. Latin America

- 10.3. Europe

- 10.4. South Asia & Oceania

- 10.5. East Asia

- 10.6. Middle East & Africa

- 11. North American Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- 12. Latin America Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- 13. Europe Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- 14. South Asia & Oceania Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- 15. East Asia Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- 16. Middle East & Africa Market Analysis 2020 to 2024 and Forecast 2025 to 2035

- 17. Market Analysis by Country

- 18. Market Structure Analysis

- 19. Competition Analysis

- 19.1. Albemarle

- 19.2. BASF

- 19.3. Clariant

- 19.4. DuPont

- 19.5. ICL

- 19.6. Italmatch

- 19.7. Lanxess

- 19.8. Nabaltec

- 20. Assumptions and Acronyms Used

- 21. Research Methodology

Don't Need a Global Report?

save 40%! on Country & Region specific reports

List Of Table

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

List Of Figures

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

- FAQs -

How big is the flame retardant coating additives industry?

The industry is anticipated to reach USD 10.18 billion in 2025.

What is the outlook on flame retardant coating additive sales?

The industry is predicted to reach a size of USD 19.61 billion by 2035.

Who are the key flame retardant coating additive companies?

Prominent players include Albemarle, BASF, Clariant, DuPont, ICL, Italmatch, Lanxess, Nabaltec, and others.

Which type of flame retardant coating additives is being widely used?

Antimony oxide types are widely used.

Which country is likely to witness the fastest growth in the flame retardant coating additives market?

China, expected to grow at 8.0% CAGR during the study period, is poised for the fastest growth.

Flame Retardant Coating Additives Market