Pigment Emulsion Market

Pigment Emulsion Industry Analysis by Source, Type, Color, End-Use, and Region through 2035

Analysis of Pigment Emulsion Market Covering 30+ Countries Including Analysis of US, Canada, UK, Germany, France, Nordics, GCC countries, Japan, Korea and many more

Pigment Emulsion Market Outlook (2025 to 2035)

The pigment emulsion market will be valued at USD 16.9 billion by 2025 end. As per Fact. MR’s analysis, pigment emulsion will grow at a CAGR of 7.6% and reach USD 38.0 billion by 2035.

In 2024, the industry underwent significant changes driven by multiple industry dynamics. The construction and automotive industries, major users of products, registered a demand surge for superior quality coatings. The demand was stimulated by higher levels of urbanization and infrastructure developments, especially across emerging economies. Producers acted by boosting capacities and innovating to keep pace with the high demand for high-quality, resilient, and high-color-strength coatings.

The textiles sector also accounted for growth in the industry, with increased demand for products owing to their higher color fastness and eco-friendliness compared to conventional dyes. The trend was specifically noticeable in the Asian Pacific region, where the production of textiles is high.

Moving forward to 2025 and beyond, the industry is expected to continue growing. The continued focus on sustainable and environmentally friendly solutions is likely to fuel innovation, with firms investing in bio-based products to comply with strict environmental regulations.

Furthermore, the development of dispersion technologies and the incorporation of nanotechnology are likely to improve product performance, responding to the changing needs of industries like construction, automotive, textiles, and cosmetics. In total, the industry will grow, fueled by both established uses and new opportunities due to changing consumer trends and industry directions.

Key Metrics

| Metrics | Values |

|---|---|

| Industry Size (2025E) | USD 16.9 billion |

| Industry Value (2035F) | USD 38.0 billion |

| Value-based CAGR (2025 to 2035) | 7.6% |

Don't Need a Global Report?

save 40%! on Country & Region specific reports

Fact.MR Survey on Pigment Emulsion Industry

Fact.MR Survey Findings: Trends According to Stakeholders (Surveyed Q4 2024, n=500 stakeholder respondents evenly divided between manufacturers, distributors, and end-users in North America, Western Europe, China, and India.)

Stakeholder Priorities

Compliance with Environmental and Safety Regulations:

- 79% of stakeholders worldwide ranked compliance with environmental and safety regulations (e.g., VOC emissions limits, REACH compliance) as a top priority.

Color Stability & Performance:

- 72% focused on the requirement for better UV and chemical resistance to support increased costs.

Regional Variance:

- North America: 65% stressed the need for water-based emulsions versus solvent-based ones due to increasing EPA regulations.

- Western Europe: 88% highlighted sustainability (bio-based pigments, reduced energy footprint), as opposed to 53% in North America.

- China/India: 59% focused on cost efficiency and scalability of mass production, and less on sustainability than Western economies.

Embracing Advanced Technologies

High Variance:

- North America: 54% of paint and coating companies incorporated automated color-matching AI systems to minimize waste.

- Western Europe: 48% applied nanotechnology to improve dispersion efficiency, with Germany (58%) leading the charge.

- China: A mere 26% utilized advanced automation due to cost concerns and a desire for bulk production techniques.

- India: 37% invested in environmentally friendly production techniques, specifically water-based products.

ROI Perspectives:

- 69% of North American stakeholders concluded that investing in automation and AI color-matching was "worth the cost," whereas only 34% in China considered it an investment.

Material Preferences & Composition Trends

Consensus:

- Acrylic-based: Preferred by 67% because of their versatility in coatings, textiles, and inks.

Variance:

- Western Europe: 52% preferred bio-based emulsions (compared to 30% worldwide), consistent with stringent EU environmental objectives.

- China/India: 46% favored hybrid recipes (acrylic + natural pigments) to strike a balance between cost and performance.

- North America: 68% opted for high-solid-content emulsions for higher coverage efficiency.

Price Sensitivity & Challenges

Shared Challenges:

- 85% mentioned increasing raw material prices (e.g., titanium dioxide, acrylic resins) as a key concern.

Regional Differences:

- North America/Western Europe: 64% were prepared to pay a 15–20% premium for sustainable and high-performing recipes.

- China/India: 76% were interested in low-cost formulations at less than $3 per liter, with just 15% willing to pay a premium.

- India: 42% indicated interest in leasing models for luxury formulations to manage costs, vs. only 22% in North America.

Pain Points in the Value Chain

Manufacturers:

- North America: 58% experienced labor shortages in specialized pigment formulation and manufacturing.

- Western Europe: 50% mentioned regulatory barriers (e.g., carbon footprint monitoring, REACH compliance).

- China: 55% had issues with raw material price fluctuations that resulted from supply chain disruptions.

Distributors:

- North America: 63% had delays in international pigment supply chains, especially from Asian vendors.

- Western Europe: 51% had to contend with low-cost Asian producers increasing competition.

- China/India: 60% had logistics issues in rural areas due to fragmented distribution channels.

End-Users (Paints, Coatings, Textile, and Ink Producers):

- North America: 44% mentioned excessive maintenance expenses for maintaining product stability over time.

- Western Europe: 40% found it challenging to adjust to new regulator-driven formulations.

- India: 55% mentioned insufficient technical support for advanced pigment systems.

Priorities for Future Investment

Alignment:

- 72% of global producers intend to invest in R&D on sustainable and bio-based emulsions for pigments.

Divergence:

- North America: 59% investing in automation and AI-based quality monitoring.

- Western Europe: 56% investing in completely carbon-neutral production processes.

- China/India: 48% investing in cost-effective high-volume production methods over premium innovations.

Regulatory Influence

- North America: 67% of stakeholders considered the strengthening EPA regulations on VOC emissions to be a key driver for water-based products.

- Western Europe: 79% considered the EU's REACH policies to be an influence driving companies towards bio-based solutions.

- China/India: Just 31% believed that regulations affected buying decisions, citing poor enforcement and cost-related decision-making.

Conclusion: Variance vs. Consensus

High Consensus:

Compliance with regulations, colour stability, and cost considerations are issues that matter worldwide.

Key Variances:

- North America: Fueling innovation with automation and AI-driven color-matching.

- Western Europe: At the forefront of sustainability via bio-based pigments and carbon-neutral processes.

- China/India: Mass production and price competitiveness-oriented, behind premium or high-technology formulations.

Strategic Insight:

A "one-size-fits-all" strategy will fail in this sector. Regional adaptation of products (e.g., bio-based in Europe, cost-effective in China, AI-based in North America) will be paramount to future penetration.

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

Government Regulations on Pigment Emulsion Industry

| Country/Region | Regulatory Impact & Mandatory Certifications |

|---|---|

| U.S. | EPA VOC Regulations: The U.S. Environmental Protection Agency (EPA) enforces limits on volatile organic compound (VOC) emissions, pushing companies toward water-based and low-VOC products. TSCA (Toxic Substances Control Act): Manufacturers must register certain chemicals used in products to comply with environmental safety standards. Mandatory Certification: ASTM D5098-02 (Standard Test Method for products in Coatings). |

| European Union | REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals): Requires manufacturers to register, test, and disclose chemical compositions for safety assessments. EU Green Deal & Carbon Neutrality Goals: These drive demand for bio-based, non-toxic products. Mandatory Certification: Ecolabel Certification for sustainable coatings and textiles. |

| China | MEE (Ministry of Ecology and Environment) Restrictions: Stricter controls on heavy metal content (e.g., lead, cadmium) products, following high-profile pollution cases. National Standards (GB/T 23986-2021): Defines quality and safety parameters for pigments used in textiles and coatings. Mandatory Certification: China RoHS Compliance (for pigments used in electronic coatings). |

| India | BIS (Bureau of Indian Standards) Compliance: Sets safety and performance criteria for products in the coatings and textile industry. CPCB (Central Pollution Control Board) Restrictions: Phasing out solvent-based emulsions in favor of water-based, non-toxic alternatives. Mandatory Certification: IS 411 (Indian Standard for product in Paints and Inks). |

| Japan | Chemical Substances Control Law (CSCL): Requires safety evaluations for all new chemicals introduced in products. JIS (Japanese Industrial Standards) Compliance: Ensures low VOC and eco-friendly pigments in paints, coatings, and textiles. Mandatory Certification: JIS K 5663 ( Water-Based Coatings). |

| South Korea | K-REACH (Korean REACH Equivalent): Similar to the EU's REACH, requiring chemical registration, safety assessments, and eco-friendly formulations. Eco-Label Certification: Encourages manufacturers to produce biodegradable and recyclable products. Mandatory Certification: KSM 6010 (Standard for Industrial Coatings). |

Market Analysis

The industry is in robust expansion, stimulated by expanding demand for environmentally friendly, high-performance coatings for various industries such as automotive, building, textiles, and packaging.

More stringent environmental regulations (e.g., VOC restrictions, REACH compliance) are propelling the trend toward waterborne and bio-based formulations, favoring forward-thinking makers that are making investments in sustainable options at the expense of low-cost, solvent-based makers. As efficiency and compliance-friendly companies capitalize on rising trends in automation, AI-based color matching, and nanotechnology, they will reap the largest industry rewards.

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

Top 3 Strategic Imperatives for Stakeholders

Invest in Sustainable Innovation

In order to get ahead of the regulatory pressures and customer demand for sustainable products, management should give highest priority to R&D of bio-based, low-VOC, and recyclable products. Investments in environmentally sustainable formulations will assure long-term competitiveness and compliance with regulations, and access growing for sustainable building materials and environmentally conscious customers.

Adopt Automation & High-Tech Solutions

With the automation and AI technologies remodeling the industry, business leaders can make it their mission to embed automated color-matching technology, IoT sensors, and nanotechnology in production flows. Embracing the escalating trend of customization and efficiency will offer a competitive advantage, particularly in areas such as North America and Western Europe, where the need for advanced high-performance solutions continues to grow.

Expand Strategic Partnerships & Global Reach

To counter supply chain disruptions and achieve regional needs, executives can leverage partnerships with prominent distributors and increase investments in emerging industry-based manufacturing facilities in areas such as India and China. Furthermore, by acquiring small yet innovative participants within the bio-based and sustainable emulsion pigment niche, scaling capabilities can be dramatically accelerated while diversified product offerings increase.

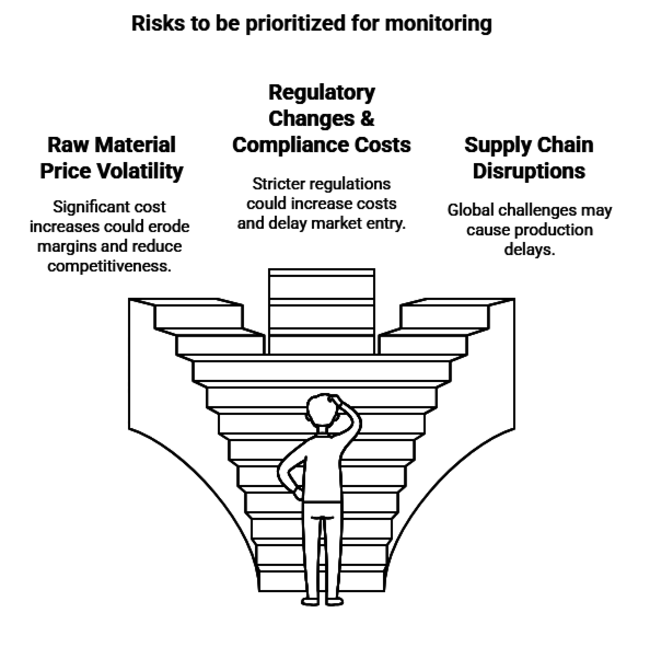

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability/Impact |

|---|---|

| Raw Material Price Volatility | High/Significant cost increases for key materials like titanium dioxide and acrylic resins could erode margins and reduce competitiveness. |

| Regulatory Changes & Compliance Costs | Medium/Stricter environmental regulations (e.g., REACH, VOC limits) could increase compliance costs and lead to delays in product development or industry entry. |

| Supply Chain Disruptions | High/Ongoing global supply chain challenges may cause delays in production, impacting the availability of key components and raw materials, especially in emerging industries. |

Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Invest in Sustainable R&D | Run feasibility studies on bio-based and low-VOC formulations to meet emerging regulatory standards and align with sustainability trends. |

| Enhance Automation & AI Integration | Initiate pilot projects to integrate AI-driven color-matching systems and IoT-enabled sensors to improve production efficiency and product customization. |

| Strengthen Global Supply Chain Resilience | Establish alternative supply sources for critical raw materials like titanium dioxide and acrylic resins to mitigate risks from ongoing supply chain disruptions. |

For the Boardroom

To stay ahead, companies in order to stay ahead in the fast-changing industry, the customer needs to step up investments in sustainable innovation, focusing on the creation of bio-based, low-VOC emulsions to address increasing regulatory pressures and consumer demand for environmentally friendly products.

The implementation of advanced automation and AI-based color-matching systems needs to be expedited to enhance production efficiency and address the increasing demand for customization in key players.

Moreover, the client must move fast to diversify its supply chain by exploring alternative sources of key raw materials, avoiding the pitfalls of volatile pricing and disruptions.

Segment-wise Analysis

By Source

Inorganic/Synthetic pigments are also more popularly applied in the pigment emulsion industry than organic pigments based on their superior color consistency, stability, and durability.

Titanium dioxide and iron oxide are less likely to degrade under UV radiation and are durable against environmental elements such as moisture and heat and are therefore highly suitable for usage in coatings and automotive and industrial paints applications.

They are also usually cheaper to manufacture and more widely distributed, helping their industry dominance.

Organic pigments are highly valued for their brightness and color and are often employed in high-end cosmetics or niche uses but can be more prone to fading and have a larger environmental footprint in some applications.

By Type

Oil-in-water (O/W) emulsions are more common than water-in-oil (W/O) emulsions because of their versatility, formulating ease, and increased application in areas like paints, coatings, cosmetics, and pharmaceuticals.

Water is the continuous phase in O/W emulsions, so they are even easier to spread, less oily, and lighter in consistency, and thus, even more applicable to cosmetics like lotions, creams, and sunscreens where a non-oily finish is desirable.

Moreover, O/W emulsions are more stable and usually more skin-friendly due to the water content, which is more pleasant for application on the skin. O/W emulsions are also easier to formulate and manufacture in bulk, as water is more plentiful and cheaper than oils.

By Color

Stock colors are more commonly utilized than specialty colors because they are cost-effective and easy to produce. Stock colors, like basic shades and popular industry colors, are easy to find and generally produced in high volumes, thus being less costly and faster to ship.

They are best for mass-market goods and sectors such as construction, automotive, and consumer goods, where consistency and uniformity throughout large quantities are critical.

In addition, the set supply chain for common colors guarantees availability and reliability, which is attractive to firms looking for efficiency and reliability in manufacturing.

By End-Use

Paint & coatings is the largest application area for pigment emulsions, owing to the extensive demand for protective, decorative, and functional coatings in a variety of industries like construction, automotive, and industrial equipment.

The worldwide construction boom and the growing automotive sector necessitate huge amounts of pigments for paints and coatings, leading to the extensive application of products.

These emulsions offer better durability, color stability, and UV resistance, which are essential in achieving long-lasting, high-performance coatings. The paint and coatings market also enjoys extensive color options and formulations, along with the capability to comply with strict regulatory requirements for VOC emissions and environmental concerns.

Country-wise Analysis

U.S.

U.S.is anticipated to witness a 7.8% CAGR in the industry during the period 2025-2035, a bit above the global average based on its strong industrial base, high demand for automotive coatings, construction paints, and consumer products. The nation's stringent environment regulations, particularly related to VOC in paints and coatings, have driven the demand for green and sustainable formulations.

EPA policies and state laws like California's Proposition 65 compel manufacturers to create compliant pigments that satisfy environmental requirements. This is leading to a shift toward waterborne and low-VOC pigment emulsions. In addition, the U.S. has a strong representation of major manufacturers like DIC Corporation and Kiri Industries, providing a secure supply chain.

UK

The UK is expected to experience a 6.4% CAGR in the industry over the next decade. This growth is driven by the construction and automotive industries, which are increasingly adopting eco-friendly and low-emission technologies due to the UK’s ambitious environmental goals.

The regulatory environment of the country, specifically the UK REACH framework, incentivizes businesses to create safer and more environmentally friendly pigments. Trade has been affected by Brexit, but the UK is still a dominant force in the international pigment industry because of its well-established manufacturing base.

Sustainability is a major driver in the UK, where low-VOC and biodegradable pigments are on the rise. This is particularly noticeable within the paint and coatings sector, where conformance with ISO 14001 (Environmental Management Standards) and other environmental qualifications are of particular importance.

France

France is expected to expand at a 6.1% CAGR in the industry for products between 2025 and 2035. France, with its dominance in the automotive and cosmetics sectors, is focusing more on sustainable formulations and environmentally friendly production processes.

Government legislations like the French National Environmental Plan and strict EU REACH regulations have also contributed much to the manufacturing of eco-friendly pigments, as producers seek to address low-VOC and non-toxic material demand.

This large consumer base in France and the luxury brand dominance enjoyed by France have increased the demand for specialty colors, particularly in the luxury cosmetics and fashion industries.

Also, France's sustainability focus in coordination with the EU Green Deal wants the whole value chain to become more eco-friendly.

Germany

Germany is expected to register a 7.2% CAGR during the industry from 2025 to 2035. As a leading world player in automotive production and industrial coatings, Germany offers high growth prospects for pigment emulsions.

The nation's emphasis on sustainability through initiatives like Germany's Renewable Energy Act (EEG) and stringent environmental regulations has initiated a growing requirement for low-VOC and environmentally friendly pigments in automotive coatings and industrial usage.

In addition, numerous innovative technology companies engaged in advanced pigment formulation are based in Germany, making the country a center of high-quality, long-lasting products.

Italy

Italy is forecasted to record a 6.0% CAGR during the period of 2025-2035 in the industry. Luxury fashion, automobile, and interior decoration sectors of Italy are pivotal drivers of demand for bespoke and eco-friendly products. Italy has traditionally been an important participant in high-end textile and cosmetics industries, and increasing demand for superior-quality pigments in specialty dyes and coatings. The nation's embracement of the EU's REACH regulations is well-suited to its drive towards sustainability and eco-friendly products.

South Korea

South Korea is projected to register a growth of 6.5% CAGR between 2025 and 2035 in the industry, underpinned chiefly by its well-developed manufacturing sector, led by automotive, electronics, and construction.

Technological upturns in South Korea at an accelerated pace, coupled with an emphasis placed on smart coating and sustainable manufacturing, provide opportunities to suppliers.

South Korea's laws are on par with international standards, and the nation has stringent environmental regulations to minimize VOC emissions in industrial coatings. This provides a stable industry for water-based and low-VOC products.

Japan

Japan will grow at a 5.8% CAGR in the industry during the next ten years. Although Japan's pigment industry is more traditional than in other parts of the world, it is still important because of its high product quality standards, requirement for specialty pigments in automotive finishes, and electronics technology.

Japan's regulations, including the Chemical Substances Control Law and food contact material legislation, guarantee strict adherence to environmental regulations, which affect pigment formulations. The trend toward sustainability is also being reflected in Japan’s shift toward eco-friendly products, especially in the automotive and construction sectors.

China

China is also anticipated to grow the most in the industry at an 8.3% CAGR from 2025 to 2035. Its fast industrialization, increasing consumer base, and rising demand for automotive and building coatings are the key drivers for growth. Being one of the world's largest manufacturing bases, China is witnessing a great transition towards sustainable and low-VOC pigments in accordance with more stringent government regulations and green building codes.

The Chinese government has also recently boosted its efforts towards minimizing environmental pollution, especially in heavy industries. This has created a boost in demand for sustainable and bio-based pigments that are compliant with China's national environmental law. China's cosmetics industry is also still expanding, creating huge demand.

Market Share Analysis

DIC Corporation: (9-10%)

Major Focus: The world leader in colorants, DIC Corporation, holds a good industry share because of its diversified product range of water-based emulsions, custom colors, and eco-friendly products. Their capacity to serve industries such as automotive, construction, and cosmetics provides them with a strong foundation. DIC's focus on sustainability is in the direction of the current trend, especially in the case of low-VOC and biodegradable pigments.

Strategic Strengths: DIC's high R&D investment in personalized products and environmentally friendly technologies is the backbone of its industry leadership. The firm enjoys its extensive distribution network, especially in North America and Asia-Pacific.

Kiri Industries Ltd (Dystar): (8-9%)

Key Focus: Being a leading player in the textile dye and industries, Kiri Industries is renowned for its high performance, especially in the automotive, plastic, and textile sectors. They have established a niche in custom colors, which is a major demand driver in various industries.

Strategic Strengths: Their focus on innovation, specifically on developing custom, eco-friendly formulations, makes them a prime candidate. The company also stands to gain from the growing demand for sustainable products in leading industries.

Sudarshan Chemicals Industries: (7-8%)

Key Strength: Sudarshan Chemicals has a significant industry presence, particularly in high-performance pigments for automotive and building coatings. The emphasis by the company on water-based emulsions and low-VOC pigments is in sync with the increasing demand for environment-friendly and long-lasting products.

Strategic Strengths: Sudarshan's dominance in specialty colors and innovation through cutting-edge pigment technology have enabled it to grow its share in the worldwide industry. Being equipped with an excellent R&D pipeline, Sudarshan stands to gain greatly from trends involving sustainability and bio-based emulsion pigments.

Huebach GmbH Composites: (5-6%)

Key Area of Concentration: Huebach GmbH deals with the industry for niche industrial uses, such as plastics and coatings. With a focus on high-performance pigments for color stability and durability, Huebach has established a firm foothold in the industry.

Strategic Strengths: Huebach's proficiency in cutting-edge pigment technology and tailor-made formulations provides it with a competitive advantage in niche applications. Huebach's solid regional presence in Asia and Europe further solidifies its share.

Pidilite Industries Ltd: (5-6%)

Major Focus: Pidilite is one of the major players in the adhesive and emulsion business with a considerable share in products for coating and paint. With its iconic brand Fevicol, Pidilite's products are seen as the best in the consumer goods, construction, and DIY segments.

Strategic Strengths: Pidilite's Indian and emerging brand strength gives it a strategic edge. The company places great emphasis on product innovation and sustainability, particularly through green products.

Key Players

- DIC Corporation

- Kiri Industries Limited

- Camex Limited

- Jupiter Dyes Pvt. Ltd.

- Kemcol Product

- Vipul Organics

- Emco Dyestuff

- Kevin Dyes & Chemicals Pvt. Ltd.

- Worldtex Speciality Chemicals

- Kanshu Chemical Industries

- Pidilite Industries Limited

- Sudarshan Chemical Industries

- Huebach GmbH

Segmentation

By Source :

With respect to the source, it is classified into organic and inorganic/synthetic.

By Type :

In terms of type, it is divided into water in oil and oil in water.

By Color :

In terms of color, it is divided into standard colors and custom colors.

By End-Use :

In terms of end-use, it is divided into paint & coatings, the textile industry, the plastic industry, the paper industry, the leather industry, and others.

By Region :

In terms of region, it is segmented into North America, Latin America, Europe, East Asia, South Asia, Oceania, and MEA.

Table of Content

- 1. Market - Executive Summary

- 2. Market Overview

- 3. Market Background and Foundation Data

- 4. Global Demand (Kilo Tons) Analysis and Forecast

- 5. Global Market - Pricing Analysis

- 6. Global Market Value (USD million) Analysis and Forecast

- 7. Global Market Analysis and Forecast, By Type

- 7.1. Glycerin

- 7.2. Ethylene Glycol

- 7.3. Propylene Glycol

- 7.4. Others

- 8. Global Market Analysis and Forecast, By End-Use Industry

- 8.1. Metalworking Industry

- 8.2. HVAC Industry

- 8.3. Automotive

- 8.4. Plastic Extrusion Process

- 8.5. Energy Production and Storage

- 8.6. Aerospace Industry

- 8.7. Others

- 9. Global Market Analysis and Forecast, By Region

- 9.1. North America

- 9.2. Latin America

- 9.3. Europe

- 9.4. East Asia

- 9.5. South Asia & Oceania

- 9.6. Middle East & Africa

- 10. North America Market Analysis and Forecast

- 11. Latin America Market Analysis and Forecast

- 12. Europe Market Analysis and Forecast

- 13. East Asia Market Analysis and Forecast

- 14. South Asia & Oceania Market Analysis and Forecast

- 15. Middle East & Africa Market Analysis and Forecast

- 16. Country-level Market Analysis and Forecast

- 17. Market Structure Analysis

- 18. Competition Analysis

- 18.1. Dynalene Inc.

- 18.2. Orison Marketing

- 18.3. Houghton

- 18.4. Salathe Oil Company

- 18.5. Star Brite, Inc.

- 18.6. Hangsterfer's Laboratories, Inc.

- 18.7. Kilfrost Limited

- 18.8. Petron Scientech, Inc.

- 18.9. Mitsui & Co. Ltd.

- 18.10. Neste

- 18.11. Bardahl

- 18.12. Master Fluid Solutions

- 18.13. Tower Metalworking Fluid

- 18.14. BDI Cooling Solutions

- 18.15. Saint-Gobain 2020

- 18.16. Total Coolants Management Solutions

- 18.17. Dynaflux Inc.

- 18.18. AMSOIL, Inc.

- 19. Assumptions & Acronyms Used

- 20. Research Methodology

Don't Need a Global Report?

save 40%! on Country & Region specific reports

List Of Table

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

List Of Figures

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

- FAQs -

How big is the pigment emulsion industry?

The industry is anticipated to reach USD 16.9 billion in 2025.

What is the outlook on pigment emulsion sales?

The industry is predicted to reach a size of USD 38.0 billion by 2035.

Who are the key pigment emulsion companies?

Prominent players include DIC Corporation, Kiri Industries Limited, Camex Limited, Jupiter Dyes Pvt. Ltd., Kemcol Product, Vipul Organics, Emco Dyestuff, Kevin Dyes & Chemicals Pvt. Ltd., Worldtex Speciality Chemicals, Kanshu Chemical Industries, Pidilite Industries Limited, Sudarshan Chemical Industries, Huebach GmbH.

Which source type of pigment emulsion is being widely used?

Inorganic/synthetic sources are widely used.

Which country is likely to witness the fastest growth in the pigment emulsion market?

China, expected to grow at 8.3% CAGR during the study period, is poised for the fastest growth.

Pigment Emulsion Market