Bio-Based Coolants Market

Bio-Based Coolants Market Analysis and Forecast by Type, End-Use Industry, and Region through 2035

Analysis of Bio-Based Coolants Market Covering 30+ Countries Including Analysis of US, Canada, UK, Germany, France, Nordics, GCC countries, Japan, Korea and many more

Bio-Based Coolants Industry Outlook (2025 to 2035)

The bio-based coolant market will be valued at USD 1.27 billion by 2025 end. As per FACT.MR's analysis, bio-based coolants will grow at a CAGR of 3.20% and reach USD 1.76 billion by 2035.

In 2024, the industry saw tremendous growth in various industries. In the automotive sector, leading manufacturers in Europe and North America have stepped up the use of coolants to meet the strict environmental regulations and consumer demand for eco-friendly vehicles.

This is due to better performance and environmentally-friendly nature of bio-based coolants.

The metalworking and HVAC industries have more widely incorporated products into manufacturing because of their inherent lubricity and high flash point, improving efficiency as well as safety.

Meanwhile, technology advances are key, with firms spending heavily on research and development to develop thermal stability and corrosion protection, making products competitive with conventional petroleum-based ones.

Looking forward to 2025 and beyond, the industry will continue on a growth path driven by a continued focus on sustainability and increasingly tough environmental regulations.

Attempts to minimize the cost of production through technology and scale economies will probably serve to alleviate one of the greatest challenges that have been discouraging mass adoption.

Furthermore, emerging industries across Asia-Pacific will present huge opportunities as these countries continue to industrialize and focus on environmental sustainability.

Ultimately, joint efforts on the part of major industry participants will be vital in driving forward product development, enhancing industry coverage, and growing awareness of the advantages of bio-based coolants.

Key Metrics

| Metrics | Values |

|---|---|

| Industry Size (2025E) | USD 1.27 billion |

| Industry Value (2035F) | USD 1.76 billion |

| Value-based CAGR (2025 to 2035) | 3.20% |

Don't Need a Global Report?

save 40%! on Country & Region specific reports

FACT.MR Survey on the Bio-Based Coolants Industry

FACT.MR Survey Findings: Trends from Stakeholder Views (Surveyed Q4 2024, n=230 stakeholder respondents evenly divided between manufacturers, distributors, industrial consumers, and automotive firms in North America, Western Europe, Japan, and South Korea)

Top Concerns of Stakeholders

Global Concerns:

- Performance & Compatibility: 43% identified thermal stability and compatibility with current engine/cooling systems as a key issue prior to the use of bio-based coolants.

Regional Variance:

- North America: 67% focused on cost efficiency, referencing the greater initial cost of products compared to petroleum-based counterparts.

- Western Europe: 90% ranked sustainability, such as biodegradability and lower carbon footprint, as a higher priority compared to 75% in the US.

- Japan/South Korea: 60% prioritized space-efficient packaging and storage solutions owing to logistics limitations, as opposed to 30% in North America.

Adoption of Sophisticated Technologies

Large Disparity in Use of Tech-Uplifted Coolants:

- North America: 55% of industrial consumers indicated trials with smart coolant monitoring systems (temperature/contamination monitoring through IoT sensors).

- Western Europe: 51% applied nanotechnology-enabled bio-based coolants, of which Germany (62%) had the highest, owing to excess R&D input in green technology.

- South Korea: 40% invested in hybrid bio-based coolants, especially in EV production, to meet high-performance thermal requirements.

Material Composition Preferences

Global Consensus:

- Vegetable Oil-Based Coolants: Preferred by 64% of stakeholders due to their biodegradability and thermal performance.

- Glycol-Based Bio Coolants: 36% opted for these in order to achieve improved freezing/boiling point stability in adverse climatic conditions.

Regional Variance:

- Western Europe: 55% opted for ester-based formulations due to superior oxidation resistance, against 28% worldwide.

- Japan/South Korea: 44% opted for hybrid formulations (bio-glycol blends) to achieve an optimal balance between cost and performance in industrial equipment.

- North America: 70% were stuck with vegetable-derived bio-coolants because of well-established supply chains in farm byproducts.

Price Sensitivity

Global Challenges:

- 87% mentioned increasing raw material prices (plant-based oils 22% higher, glycol-based materials 15% higher) as a leading issue.

Regional Willingness to Pay Differences:

- North America/Western Europe: 60% would tolerate a 15–20% premium for performance-improved bio-based coolants.

- Japan/South Korea: 75% looked for low-price options (below USD 6/liter), with only 14% willing to pay premiums.

- South Korea: 47% favored subscription/leasing schemes for industrial coolant supply to counterbalance exorbitant initial costs.

Supply Chain & Value Chain Pain Points

Manufacturers:

- US: 53% experienced issues with sourcing non-GMO plant-based raw materials because of supply chain limitations.

- Western Europe: 50% were hindered by regulatory approval lead times, which delayed new product introductions.

- Japan: 58% indicated low demand resulting from industrial reluctance to shift from synthetic coolants.

Distributors:

- North America: 65% mentioned unstable import/export tariffs on bio-based raw materials as a major concern.

- Western Europe: 56% were confronted by cheaper Asian competition supplying synthetic substitutes.

- Japan/South Korea: 62% mentioned rural distribution inefficiencies in logistics, hindering take-up.

End-Users (Automotive & Industrial Users):

- US: 45% mentioned high maintenance costs in making the shift to products for aged engines.

- Western Europe: 40% grappled with the retrofitting of industrial cooling systems to be bio-coolant capable.

- Japan: 55% did not have technical assistance/support from manufacturers in adopting bio-coolants.

Investment Priorities in the Future

Alignment Between Regions:

- 76% of worldwide manufacturers intend to invest in R&D to enhance the performance of bio-coolants and reduce costs.

Divergence in Investment Direction:

- North America: 60% invested in creating hybrid bio-synthetic coolants with improved performance in automotive & industrial uses.

- Western Europe: 58% invested in net-zero emission manufacturing (e.g., renewable energy-based manufacturing).

- Japan/South Korea: 50% are concerned with compact, long-life designs for EV and robotics cooling applications.

Regulatory Impact on Growth

- North America: 67% of respondents mentioned EPA's Renewable Coolants Initiative as a disruptor, raising compliance expenses.

- Western Europe: 83% saw the EU's 2024 Green Manufacturing Directive as a driver for bio-coolant growth.

- Japan/South Korea: Just 30% believed regulations had a significant influence on buying decisions, attributing this to less stringent enforcement mechanisms.

Conclusion: Key Variances vs. Consensus

High Consensus:

Universal concerns are environmental compliance, thermal performance, and cost pressures.

Critical Variances:

- North America: Cost-performance balance-driven growth vs. Japan/South Korea: Reluctant adoption because of cost considerations.

- Western Europe: Sustainability leadership & regulation-driven demand vs. Asia: Hybrid cost-effective solutions.

Strategic Insight:

A one-size-fits-all solution will not suffice. Regional adaptation (e.g., vegetable-based coolants in North America, ester-based in Europe, and hybrid blends in Asia) is the key to penetration.

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

Government Regulations on the Bio-Based Coolants Industry

| Country/Region | Policies, Regulations, & Certifications |

|---|---|

| U.S. |

|

| European Union |

|

| Germany |

|

| France |

|

| UK |

|

| China |

|

| Japan |

|

| South Korea |

|

| India |

|

Market Analysis

The industry is on a steady upward trend, fueled by mounting environmental regulations, growth in demand for sustainable industrial products, and advances in high-performance bio-coolant formulations.

Automotive, industrial machinery businesses, and environmentally aware consumers are poised to benefit as regulatory support and technology breakthroughs enhance product uptake. Conventional petroleum-based coolant producers, however, risk losing industry share unless they keep pace with the transition to bio-based products.

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

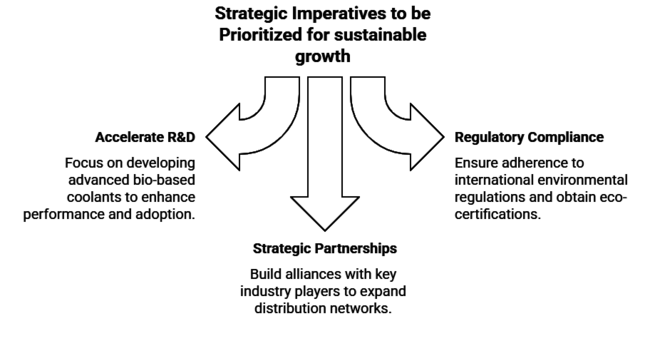

Top 3 Strategic Imperatives for Stakeholders

Speed Up R&D for Performance-Oriented Bio-Based Coolants

Actionable Recommendation: Invest in second-generation products with improved thermal stability, corrosion, and compatibility with current engine and industrial systems to push performance limits and induce adoption.

Follow Regulatory & Sustainability Trends

Actionable Recommendation: Remain compliant with international environmental regulations (EU Green Deal, EPA norms, REACH, etc.) and obtain eco-certifications (e.g., USDA BioPreferred, EU Ecolabel) to enhance positioning and remain competitive.

Grow Strategic Partnerships & Distribution Networks

Actionable Advice: Partner with automakers, industrial OEMs, and fleet operators while building supply chain robustness to leverage increasing demand for sustainable cooling solutions in strategic industries such as North America, Europe, and Asia-Pacific.

Top 3 Risks Stakeholders Should Monitor

| Risk | Probability/Impact |

|---|---|

| High Raw Material Costs & Supply Chain Disruptions | Medium-High |

| Slow Adoption Due to Performance & Cost Concerns | Medium |

| Regulatory Uncertainty & Policy Shifts | Medium |

1-Year Executive Watchlist

| Priority | Immediate Action |

|---|---|

| Scaling Production Efficiency | Conduct a feasibility study on cost-effective bio-glycol sourcing and alternative raw materials to mitigate supply chain risks. |

| Validation & OEM Adoption | Initiate an OEM feedback loop to assess performance concerns and drive pilot testing programs for products in key industries (automotive, heavy machinery, data centers). |

| Channel Expansion & Growth | Launch a distributor incentive program to accelerate adoption through fleet operators, industrial users, and auto service providers. |

For the Boardroom

To stay ahead, companies need to remain ahead of the curve in the industry, The company will need to step up R&D investment in high-performance formulations, tighten regulatory alignment, and build OEM and alliances.

With sustainability regulations becoming increasingly stringent and industrial users looking for cost-effective, high-efficiency alternatives, a two-pronged strategy of product innovation and industry education will be essential.

Near-term next steps involve securing strategic raw material supply sources, initiating pilot programs with major OEMs, and scaling distribution incentives to drive adoption.

This insight redirects the roadmap toward value-driven differentiation, supply chain resilience, and active engagement with policymakers and industry leaders to ensure long-term industry leadership.

Segment-wise Analysis

By Type

Ethylene Glycol (EG) is the most common base coolant because of its high thermal conductivity, lower viscosity, and cost savings over glycerin and propylene glycol.

It is an effective heat transfer fluid, and hence, it is the most used in automotive, industrial, and HVAC applications.

Nevertheless, its extreme toxicity is of environmental and safety concern, prompting greater regulatory oversight. Propylene Glycol (PG) is taking advantage as safer and non-toxic, primarily for food preparation and environmentally critical use, even if it performs less efficiently as a heat conductor.

By End-Use Industry

Automotive industry is the most significant for bio-based coolants user motivated by the demands of the effective cooling of engines, emissions regulatory forces, and EV transition.

EG and PG traditional coolants exhaust internal combustion engines, whereas EVs demand application-specific dielectric coolants in battery thermal management.

The HVAC sector also utilizes coolants for heat pumps, chillers, and refrigeration systems, but its transition to bio-based options is slower because efficiency levels are strictly enforced.

Metalworking, plastic extrusion, aerospace, and energy storage have heat-dissipating coolants used in them, but not at the same volumes as the automotive industry.

While with growing sustainability norms, automobile makers are pioneering a transition toward low-toxicity, bio-based coolants and hence make up the core motive of the industry's growth.

Country-wise Analysis

The U.S.

The bio-based coolants industry in the US will register a CAGR of 3.4% during the period 2025 to 2035, marginally higher than the global average, due to more stringent environmental regulations, growing EV penetration, and industrial sustainability efforts.

Initiatives like the EPA's Renewable Coolants Initiative and California's Proposition 65 are compelling manufacturers to adopt low-toxicity, biodegradable coolants.

The automotive industry is the largest user, and demand is increasing for EV battery thermal management systems.

The metalworking and HVAC industries are also moving toward bio-based alternatives, especially propylene glycol-based products, because they are low in toxicity and high in performance.

Some of the major challenges are that the raw material is expensive and there is opposition from incumbent coolant makers.

But government grants under the USDA BioPreferred Program and corporate encouragement for carbon neutrality will propel the industry further.

Players in the United States are already investing in leading-edge coolant formulators that achieve higher heat transfer efficiency while respecting strict environmental constraints.

UK

The UK industry will grow at a CAGR of 3.1% from 2025 to 2035, driven by net-zero targets, rigorous vehicle emissions regulations, and the growth of green industrial policies.

The UK REACH system still controls harmful chemicals in coolants, which is driving manufacturers towards bio-based products. The automotive sector, and the EV segment in particular, is one of the fastest-growing drivers with the UK's transition from ICE vehicles by 2035.

The HVAC sector is shifting towards more environmentally friendly refrigerants and heat transfer fluids, which create demand for bio-based refrigerants. Cost sensitivity and insufficient domestic production capability remain concerns, however.

British-based manufacturers are focusing on high-performance, biodegradable coolants to meet government incentives and corporate sustainability targets.

Strategic partnerships with automotive makers, energy storage firms, and industrial equipment manufacturers are the primary drivers for broader adoption.

France

The French industry is anticipated to grow at a CAGR of 3.2% between 2025 and 2035, fueled by EU Green Deal policies, circular economy legislation, and AGEC law on sustainable industry operations.

The French automotive sector, home to Renault and Stellantis, is investing heavily in bio-based thermal management systems, especially for use in EV batteries.

The HVAC industry is also transitioning towards green refrigerants and cooling fluids, driving further demand. Government industrial decarbonization incentives are compelling metalworking, plastic extrusion, and power generation industries to move from petroleum-based coolants to bio-based coolants.

The major challenges are high production costs and performance validation demands in industrial usage. However, French leadership in renewable energy and sustainability makes the country an interesting industry for bio-coolant adoption across various industries.

Germany

Germany is expected to expand at a CAGR of 3.5% from 2025 to 2035, driven by car electrification, stringent EU chemical safety rules (REACH), and advanced industrial cooling requirements.

Germany is heavily investing in EV battery cooling technology with leading vehicle manufacturers like Volkswagen, BMW, and Mercedes-Benz having their headquarters there and therefore the center of demand for bio-based coolants.

Aerospace and metalworking applications also require environmentally benign, high-performance coolants as regulations surrounding harmful substances increasingly get stricter.

The Blue Angel (Blauer Engel) environmental prize is promoting the application of non-toxic and biodegradable coolants. German industry leads R&D of premium formulations, especially glycerin-based and hybrid coolants with both thermal performance and ecological benefits. Excessive production costs remain a problem, but governmental incentives for environmentally friendly industrial products continue to stimulate growth.

Italy

Italy's manufacturing will have a CAGR of 3.0% for 2025 to 2035, spurred by EU-level environmental policies and increasing pressure toward greener manufacturing practices. Italy's automotive sector, led by Ferrari, Fiat, and Lamborghini, is adding bio-based coolants to high-performance vehicles and electric vehicles.

The industrial sector, including plastic extrusion and metalworking, is gradually moving toward green thermal management solutions, though uptake trails behind Germany or France.

The focus of the Italian government on green technology and energy efficiency is expected to propel investments in bio-based cooling solutions. However, cost-sensitive customers and sluggish industrial uptake are barrier factors.

South Korea

South Korea's industry is likely to expand at a CAGR of 2.9% from 2025 to 2035, driven by the country's EV boom (Hyundai, Kia), semiconductor cooling needs, and government-backed sustainability efforts.

The Korean Green Certification encourages the adoption of bio-based thermal management technology, especially for EV batteries and data center cooling. The HVAC industry is also a growing customer, although it lags in the cost sensitivity context. Government pressure toward green technology exports and environmentally friendly manufacturing is expected to spur further growth.

Japan

Japan's industry is set to register a CAGR of 2.8% during 2025 to 2035, marginally lower than the world average, against cost-conscious industrial buyers and negligible regulatory pressure compared to Europe.

The automotive segment (Toyota, Honda, Nissan) is, however, gradually embracing products in hybrid and electric vehicles.

The Japanese HVAC industry is also shifting towards low-toxicity, eco-friendly refrigerants but slow to embrace due to cost. Coolants adhere to the JIS K2234 standard, but bio-based coolants have not become popular with mass consumers in industry.

China

China industry is expected to develop with the highest CAGR of 3.6% between 2025 to 2035 based on swift growth of EVs, strict green regulations, and industrialization initiatives.

As the world's largest car producer, China has made significant investments in the bio-based thermal management system for its rapidly growing hybrid car and electric car industries.

National Green Product Certification is promoting the adoption of green cooling technologies, and government subsidies for green production are driving demand. The HVAC industry is also a strong growth driver, especially for commercial-scale refrigeration and district cooling facilities. Strong carbon neutrality ambitions by the Chinese government are about to unlock huge investments in green coolants.

Industry Share Analysis

Dynalene Inc. (6.1%)

Dynalene Inc is the leading provider of high-performance bio-based coolants, particularly for industrial, energy storage, and HVAC applications.

Dynalene has a strong R&D focus, always pushing itself to enhance thermal conductivity and reduce the environmental impact. Dynalene bio-glycol and hybrid coolants have widespread uses in renewable energy products, industrial cooling systems, and EV battery coolants.

It maintains its industry leadership because it is able to tailor formulas to specific industry requirements and is thus better liked by the high-performance niche applications.

Orison Marketing (5.5%)

Orison has established a solid North American presence concentrated on non-toxic, biodegradable automobile, HVAC, and energy storage coolants. Orison gained shares by penetrating the electric vehicle and renewable energy industries, in which low toxicity and eco-sustainability are issues of utmost priority. With its growing pipeline of green cooling liquids, Orison is benefiting from increasing regulatory thrust away from petro-based coolants.

Houghton (Quaker Houghton) (4.7%)

Houghton, a Quaker Houghton company, is an industrial fluid distributor with a strong global footprint. The firm is leveraging its scale and distribution system to increase penetration in the bio-based coolant industry.

Houghton has a dominant position in metalworking fluids and industrial coolants and distributes bio-based products to manufacturing, aerospace, and heavy equipment industries.

Its global manufacturing footprint and low-cost manufacturing capabilities make it a player in competing on high-volume applications.

Kilfrost Limited (4.4%)

Kilfrost is a pan-European leader in biodegradable coolants with a strong focus on aerospace and rail industry segments.

Kilfrost has strong positioning in the European landscape, where high environmental standards and sustainability objectives drive the demand for coolants that are non-toxic and glycol-free.

Kilfrost's low-temperature bio-based coolants expertise makes it the supplier of choice in aviation de-icing fluid applications, rail cooling plant, and industrial refrigeration.

Petron Scientech, Inc. (3.8%)

Petron Scientech is a biochemical solutions company with increasing operations in the Asia-Pacific region. It has a strong presence in the automotive and industrial cooling industries, where its bio-based ethylene glycol (EG) and propylene glycol (PG) coolants are gaining momentum.

Petron Scientech is developing biorefinery technology to enhance its capacity and enhance its industry position within developing economies like China and India, where demand for green coolants is on the rise.

Key Players

- Orison Marketing

- Houghton

- Salathe Oil Company

- Star Brite, Inc.

- Hangsterfer's Laboratories, Inc.

- Kilfrost Limited

- Petron Scientech, Inc.

- Mitsui & Co. Ltd.

- Neste

- Bardahl

- Master Fluid Solutions

- Tower Metalworking Fluid

- BDI Cooling Solutions

- Saint-Gobain 2020

- Total Coolants Management Solutions

- Dynaflux Inc.

- AMSOIL, Inc.

Segmentation

By Type :

With respect to the type, it is classified into glycerin, ethylene glycol, propylene glycol, and others.

By End-User Industry :

In terms of end-user industry, it is divided into metalworking industry, HVAC industry, automotive, plastic extrusion process, energy production and storage, aerospace industry, and others.

By Region :

In terms of region, it is segmented into North America, Latin America, Europe, East Asia, South Asia, Oceania, and MEA.

Table of Content

- 1. Market - Executive Summary

- 2. Market Overview

- 3. Market Background and Foundation Data

- 4. Global Demand (Kilo Tons) Analysis and Forecast

- 5. Global Market - Pricing Analysis

- 6. Global Market Value (USD million) Analysis and Forecast

- 7. Global Market Analysis and Forecast, By Type

- 7.1. Glycerin

- 7.2. Ethylene Glycol

- 7.3. Propylene Glycol

- 7.4. Others

- 8. Global Market Analysis and Forecast, By End-Use Industry

- 8.1. Metalworking Industry

- 8.2. HVAC Industry

- 8.3. Automotive

- 8.4. Plastic Extrusion Process

- 8.5. Energy Production and Storage

- 8.6. Aerospace Industry

- 8.7. Others

- 9. Global Market Analysis and Forecast, By Region

- 9.1. North America

- 9.2. Latin America

- 9.3. Europe

- 9.4. East Asia

- 9.5. South Asia & Oceania

- 9.6. Middle East & Africa

- 10. North America Market Analysis and Forecast

- 11. Latin America Market Analysis and Forecast

- 12. Europe Market Analysis and Forecast

- 13. East Asia Market Analysis and Forecast

- 14. South Asia & Oceania Market Analysis and Forecast

- 15. Middle East & Africa Market Analysis and Forecast

- 16. Country-level Market Analysis and Forecast

- 17. Market Structure Analysis

- 18. Competition Analysis

- 18.1. Dynalene Inc.

- 18.2. Orison Marketing

- 18.3. Houghton

- 18.4. Salathe Oil Company

- 18.5. Star Brite, Inc.

- 18.6. Hangsterfer's Laboratories, Inc.

- 18.7. Kilfrost Limited

- 18.8. Petron Scientech, Inc.

- 18.9. Mitsui & Co. Ltd.

- 18.10. Neste

- 18.11. Bardahl

- 18.12. Master Fluid Solutions

- 18.13. Tower Metalworking Fluid

- 18.14. BDI Cooling Solutions

- 18.15. Saint-Gobain 2020

- 18.16. Total Coolants Management Solutions

- 18.17. Dynaflux Inc.

- 18.18. AMSOIL, Inc.

- 19. Assumptions & Acronyms Used

- 20. Research Methodology

Don't Need a Global Report?

save 40%! on Country & Region specific reports

List Of Table

More Insights, Lesser Cost (-50% off)

Insights on import/export production,

pricing analysis, and more – Only @ Fact.MR

List Of Figures

Know thy Competitors

Competitive landscape highlights only certain players

Complete list available upon request

- FAQs -

How big is the bio-based coolants industry?

The industry is anticipated to reach USD 1.27 billion in 2025.

What is the outlook on bio-based coolant sales?

The industry is predicted to reach a size of USD 1.76 billion by 2035.

Who are the key bio-based coolants companies?

Prominent players include Orison Marketing, Houghton, Salathe Oil Company, Star Brite, Inc., Hangsterfer's Laboratories, Inc., Kilfrost Limited, Petron Scientech, Inc., Mitsui & Co. Ltd., Neste, Bardahl, Master Fluid Solutions, Tower Metalworking Fluid, BDI Cooling Solutions, Saint-Gobain, Total Coolants Management Solutions, Dynaflux Inc., AMSOIL, Inc.

Which industry uses bio-based coolants the most and why?

Automotive industry is the most significant end-user for bio-based coolants, motivated by the demands of the effective cooling of engines, emissions regulatory forces, and EV transition.

Which country is likely to witness the fastest growth in the bio-based coolants market?

China, expected to grow at 3.6% CAGR during the study period, is poised for the fastest growth.

Bio-Based Coolants Market